We were deeply concerned late last year when the RBI-Government fracas was out in the open and we outlined our view through this article titled RBI Under Attack, which was written in the backdrop of Dr. Viral Acharya’s independence speech in October 2018, the controversial RBI Board meeting in November 2018, and Dr. Patel’s resignation in December 2018. Apart from opining on the issue of RBI’s independence, we compared the Balance sheet of the RBI with other global central banks to determine if and whether the RBI indeed has excess capital (See Table 2, Below.)

We are glad to note the recommendations of the Jalan Committee report on the framework to determine the economic capital of the Reserve Bank of India. We have to always keep in mind that India remains an Emerging Market country with its own macro frailties and a government which runs a fiscal deficit on whom the RBI cannot depend on capital infusion if things go bad. The RBI thus needs to have its own sufficiently large capital buffer.

The Jalan committee, I believe, has put this matter to rest by laying down the following:

1. Any Surplus due to the government can be paid only from retained earnings and not by using the notional revaluation reserves.

2. The Contingent capital buffer has to remain at all times in a band of 5.5% - 6.5% of the RBI’s total balance sheet

3. The total economic capital of the RBI needs to be in the range of 20% - 24.5% of the RBI’s total balance sheet

The Point no.1 follows the normal accounting prudence of paying dividend only out of income and profit earned and not by profit accrued but not realized which shows up as Revaluation Reserves in RBI’s balance sheet, as explained in detail in our article link above.

Point no.2, is where the 52,637 crs has emanated from as the Board of the RBI decided to keep the Contingency Capital at the lower band of 5.5% and hence paid out the excess to the government. This also means that for it to pay it again, the contingency capital would have to rise above towards the 6.5% level for a fresh surplus to be transferred. This is why we believe this capital transfer to be a ‘one-time’ in nature.

Point no.3 details how the annual dividend of the RBI will be paid. For every year, if the economic capital is between the 20% -24.5% ranges, the entire annual surplus can be paid out to the government as dividend. This explains the INR 1,23,414 cr annual dividend for the period July 2018- June 2019. If there is no major movement in the market risk, credit risk and currency, one can expect that the RBI will be able to transfer a large part of its surplus to the government every year.

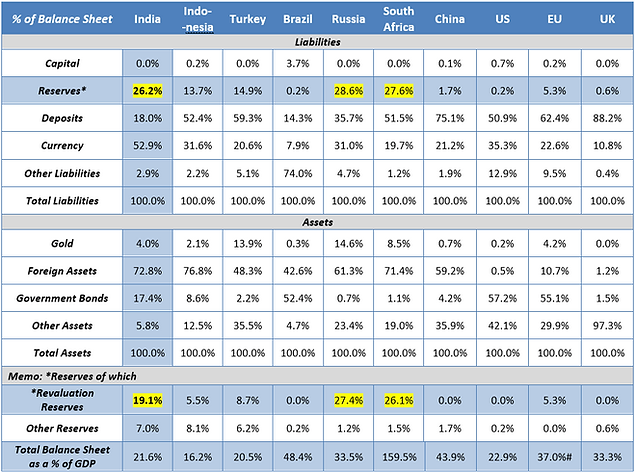

Table 2: RBI does have excess reserves, but those are not cash reserves

Source: Annual Reports of Central Banks, Classification into items is as per the authors understanding; # Euro GDP is of 19 countries which use the EURO as a Currency; Data for India is as of June 2018; UK is February 2018, rest all is as at December 2017

Arvind Chari is Head Fixed Income & Alternatives at Quantum Advisors Pvt. Ltd (QAPL).

Quantum Advisors is an India Based, India Focused, Investment Management Institution managing money for North American and European Pensions, Sovereign Wealth Funds, Endowments, Wealthy Individuals across Indian Equity, Fixed Income and Real Estate*.

*Real Estate is managed through Primary Real Estate, an Associate of Quantum Advisors.

Disclaimer:

· Quantum Advisors Private Limited is registered in India and holds a Portfolio Management License from Securities and Exchange Board of India (SEBI), India. It is also registered with the Securities Exchange Commission, USA as an Investment Adviser and as a Restricted Portfolio Manager with the Canadian provinces of British Columbia (BCSC), Ontario (OSC) and Quebec (AMF). Registration with the said authorities does not imply any level of skill and training.. This summary is subject to a more complete description and does not contain all of the information necessary to make an investment decision, including, but not limited to, the risks, fee and investment strategies of QAS. Any offering will be made only pursuant to an offering memorandum and other relevant documents that will be made available to qualified purchasers under applicable securities laws, and these documents must be carefully reviewed before any investment is made.

· Investing in shares or any asset is a risky proposition and share prices or prices of any assets can increase or decrease in value.

· Investors wishing to ‘double their money’ in one year or having short-term return objectives should not seek the advice of QAS as the research and investment style followed by QAS typically considers a longer-term time horizon.

· All of the forward-looking statements made in this communication are inherently uncertain and QAPL cannot assure the reader that the results or developments anticipated by QAPL will be realized or even if realized, will have the expected consequences to or effects on, us or our business prospects, financial condition or results of operations. A prospective investor can generally identify forward-looking statements as statements containing the words “will”, “should”, “can”, “may”, “believe”, “expect”, “anticipate”, “intend”, “contemplate”, “estimate”, “assume”, “target”, “targeted” or other similar expressions. Readers are cautioned not to place undue reliance on these forward-looking statements in making any investment decision. Forward-looking statements made in this communication apply only as of the date of this communication. While we may elect to update forward-looking statements from time to time, we specifically disclaim any obligation to do so, even if internal estimates change, unless otherwise required by applicable Securities laws.

· The views expressed here in this document are for general information and reading purpose only and do not constitute any guidelines and recommendations on any course of action to be followed by the reader. The views are not meant to serve as a professional guide / investment advice / intended to be an offer or solicitation for the purchase or sale of any financial product or instrument. Information sourced from third parties cannot be guaranteed or was not independently verified. Whilst no action has been solicited based upon the information provided herein, due care has been taken to ensure that the facts are accurate and views given are fair and reasonable as on date.