A Decisive Mandate

Quantum Advisors India

Building your India portfolio since 1990 on a foundation of ethics, integrity & disciplined investment research process.

May 5, 2014Not since 1984, has India voted so decisively in favor of a single party.

The congress party then, on a post Indira Gandhi assassination sympathy wave, won a massive 400 seats.

Today the BJP and its coalition NDA; led by Narendra Modi and his campaign of Hope; Aspirations; Decisiveness; is all set to form a majority government with more than 330 seats out of the 543 seats. This is significant in many ways.

- The BJP on its own is slated to cross the simple majority of 272. Arithmetically, it can do away with all its allies and still provide a stable single party majority government for the next 5 years. This is the biggest development.

- Coalition government has been seen as a bane of Indian politics in terms of the government's ability in taking tough decisions. Although, on a GDP growth basis, even in coalition government, the growth has been at or above the long term average; but the push and pull of coalition does lead to instability and compromise. A clear majority government would mean that for the next 5 years; the BJP and its allies can lay out their policies and run the government without worrying about the stability of the government.

- The result also shows an actual decimation of the ruling Congress party. They seem like they won't cross even the 50 mark (they had won more than 200 seats in 2009). And what is unbelievable and potentially dangerous in a democracy; is that in the lower house; there won't be any leader of opposition. The second largest party needs to have at least 55 seats to claim the position of the leader of opposition. That seems unlikely in the current juncture. Such is the margin of this BJP victory.

- Along with the congress, which is centre to the left party; even the communist party has been decimated in their home ground of West Bengal; winning only 1 Seat. The BJP is evidently a centre to right party. Time will tell whether this is beginning of the BJP making its presence in traditional Left support base in Eastern India. And how does India, a socialist country, accept and deal with a right wing ; pro capitalism party at the centre.

Expectations from the BJP government would be sky high. It has been seen in the Equity markets with the Sensex touching record highs prior to the outcome. Today, as the leads came through, the sensex at one time was up more than 6%; but profit booking since has led to the gain restricted to around the 1% mark. The RBI also seems to have been extremely active in buying the flood of Dollars. The INR still comfortably broke through the 59 mark and traded as low as INR 58.62/USD. It seems to be settling around the 59/$ mark. As mentioned many time before, we expect the RBI to very strong buyers of the $ at all levels below the INR=60/$.

Modi a lesser messiah for the bond market

The bond market did not enter the outcome with any major positioning. Although when seen from the high point of yield in April of 9.12%; the current 10 year yields @ 8.78% looks low; but when seen from a broader perspective; the long bond yields have ranged between the 8.70% and 9% mark broadly in the last 2-3 months. Today, the bond yields did drop sharply to trade below 8.7%; but profit booking and a muted auction result has got the market to trade back at the 8.75% - 8.80% band.

The bond market is staring at the reality of excess net supply; chances of EL NINO impacting inflation and a budget outcome which could see a higher fiscal deficit and hence a higher borrowing number for the market. Even a strong Modi government cannot wish away this reality for the bond market and hence we still see a fairly range bound bond market. Only a lowered threat of EL NINO; drop in food inflation and stable INR will lead to a lower bond yields.

The new government would also take over a very weak economy. With no pick up in industrial activity; high bad loans in the banking system; over leveraged corporates and very little capex activity. Add to that a fiscal situation which is lower only because of some pure arithmetic trickery and ruthless cuts in needed spending. Given this, if I were the Finance minister of a strong government in its first budget; I would first clean up the fiscals. And thus an assumption of a 4.1% / GDP fiscal deficit looks highly improbable. The government banks require some immediate recapitalization and subsidy arrears need to cleared; and we thus pencil in an increase in the fiscal deficit of about 0.5% to take it back to 4.6% of GDP. This if well communicated shouldn't be any issue with the rating agencies also.

The next big event after the government formation would be the expectation from the budget (expected some time in July). Till then, markets would move back to focusing on domestic realities and the global developments.

Related Post

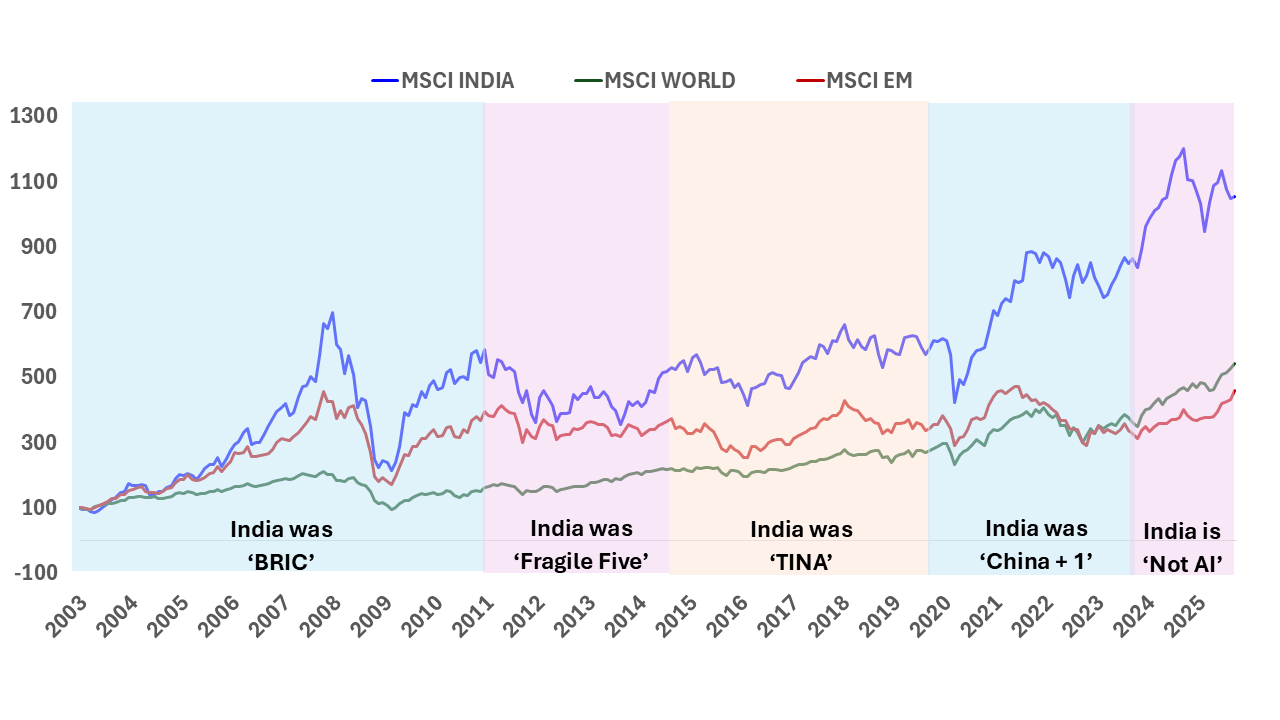

India: T I N A to A N T I

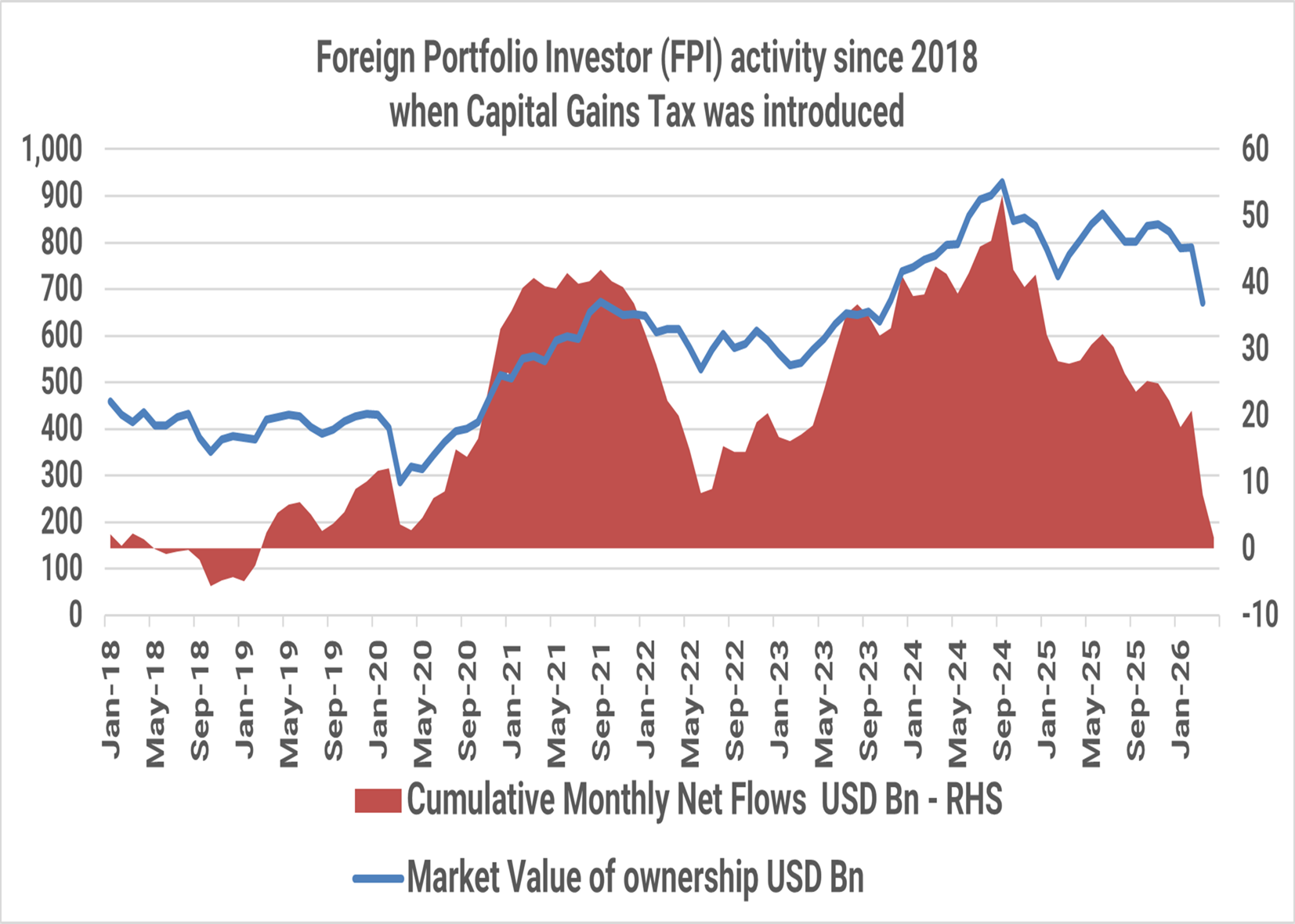

The Indian public equity markets peaked in September 2024. Since then, foreign investors have sold USD 51 billion till April 2026. The market value of foreign investor holding in Indian equities has fallen from USD 930 billion in September 2024 to USD 670 billion, a ~30% drop as at the end of March 2026.

India Investing: From a complicated 2025 to a Simpler 2026?

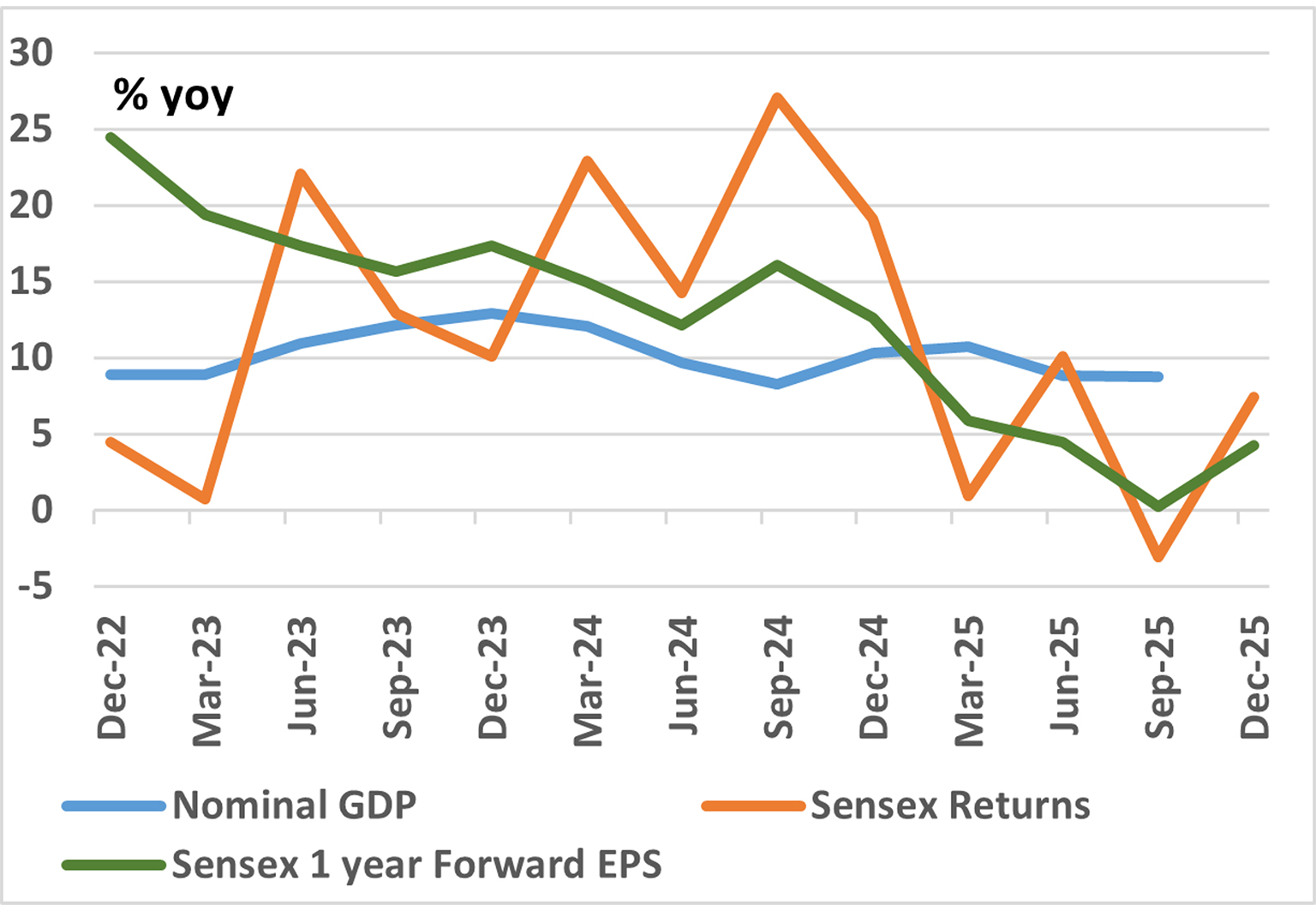

The simple India investing story of double-digit nominal GDP growth reflecting in stock market returns even in dollar terms has faced some headwinds in 2024/2025. Are these headwinds structural? What should investors expect in 2026?

India Investing Under Global Mood Swings

The narrative around global investing is often built around stories. Investors weave these stories around cycles, themes, and opportunities to justify and support their investment rationale.

The Great India Under-Allocation

The most common response to our reach outs to prospective Global Investors to get them interested in Indian Equities is ‘NO’ response.

Our Strategies

Explore how our two main strategies – Predictable India Equity and India Integrity Equity - with demonstrated success of our tried and tested research and investment processes can ensure your India equity allocation will have higher predictable outcomes and no surprises.

Q India Value Equity Strategy

20+ years of India Long-only, Liquid, High-Governance, Margin of safety = Predictability

Integrity screen since 1996, strategy Track record since 2000.

Q India Responsible Returns Strategy

Liquid, proprietary Integrity Scores, Financial Soundness

Integrity Screen since 1996, enhanced criterion since 2015, strategy Track Record since 2019; strategy AuM: $9.7 mn Mandate Capacity: $5 billion

Quantum Advisors pioneered a quantitative as well as qualitative analytical approach to equity investing in India, providing for the first time, consistently applied valuation metrics to evaluate investment opportunities in India’s emerging stock markets. Over the years, Quantum Advisors has continued and enhanced its tradition of extensive financial analysis and value investing, as it has evolved into an investment advisor and asset manager.

Our investment philosophy and strategy involves the use of intensive qualitative and quantitative fundamental analysis. We build and monitor our clients’ portfolios actively while at the same time avoiding excessive trading, and control risk by endeavoring to keep our clients’ portfolio adequately diversified, both in terms of the sectors included in those portfolios, as well as with respect to the level of concentration in any specific security.