Has India Got its Funk Back?

Quantum Advisors India

Building your India portfolio since 1990 on a foundation of ethics, integrity & disciplined investment research process.

Aug 5, 2013The irrational exuberance of the go-go years of the BRIC fairy tale has given way to irrational dejection.

The irrational exuberance of the go-go years of the BRIC fairy tale has given way to indigestion - and we seem to be on the verge of irrational dejection.

The general disappointment with “lack of policy making” in the BRICs coupled with the foot-off-the-pedal remark from US Federal Reserve Chairman Ben Bernanke has resulted in angst over India's future. A cover page story in The Economist, a magazine, blared “How India got its funk”. The headline - and the story - should have focused on the other aspect of the equation: how foreign investors approached India the way a love-struck teenager swoons over a freckled, bespectacled school girl with braces. Like the school girl, India had this known 3-pronged problem of a fiscal deficit, a current account deficit, and inflation. But love-struck investors did not price that in. And, when they these problems became apparent, they fled the object of their desire and spread malicious rumours about the young lady. Using that parody, the rapid decline in the INR - some 20% beyond the levels suggested by the theoretical Real Effective Exchange Rate (REER) - is “logical”.

To be fair, India's rapid fall from grace is not solely due to a “misjudged expectation” of the foreign investor. Irrational exuberance can only occur when there is some rational exuberance to begin with. The irrationality comes later.

The rational exuberance was there early in the cycle. Like little puppy dogs cuddled and coddled by the “where is my next commission?” line-up of global investment banking firms, the Dream Team of India's reforms represented by Prime Minister Singh, Finance Minister Chidambaram, and Deputy Chief of the Planning Commission Montek Singh Ahluwalia - ably supported by a list of puppets from the Congress party and the bureaucracy - were happy to head on global road shows and high altitude summits at Davos. Their missions: “talk up” India. With their western education and polished English, they wowed the uniformed. India was one of the largest recipients of foreign flows.

A sign of irrationality: Capital good companies which typically work on wafer thin margins, high reliance on working capital financing, and performance guarantees that can extend for years were trading at 4x Price to Book. Hey, India was Shining and India was Resurgent and these companies were worth every over-priced dime.

A rising stock market makes good headlines - and allows the rubbish to get swept under the carpet. In fact, it allows more rubbish to be created only to be hidden again. So many of the well-travelled and well-quoted captains of industry gamed the willing-to-be-greased system. They played to the full-house gallery of “India is a super power” fans. In doing so, India's legendary list of suspects built up their personal - mostly questionable - wealth. The freckled, bespectacled schoolgirl with braces turned out to be the head of an over ground, legitimate enterprise that would make the Colombian drug lords weep with shame.

India 101: It's real, pinch it

Within this Love Boat mentality, the more rational views were submerged. India, we argued:

- Would not sustain long term growth rates of 8% plus, a 6.5% to 7% long term rate was more rational;

- While there was an infrastructure story, there was also a distortion of costing; national assets (coal, gas, iron ore, real estate, spectrum) were being given away at throw away prices to a favoured few and would not stand the test of changed government regimes - or of court challenges;

- While Goldman was pushing its “demographic dividend” xl sheet, we argued that there was no job creation to actualise that flawed expectation; in fact, that may be a liability and - in our view - the real risk to the “India story”;

- While there is the case for a surge in consumption due to rising rural and urban incomes, the naïve Indian businessmen - fuelled by cheap and plentiful credit - were over reaching themselves with mall construction or even IT office space;

- Despite all the heroics at Davos, the reality is that India was a work-in-progress economy for the next 20 years; the reality of feeding 200 million poor and helping them climb up the economic ladder would result in fiscal deficits, higher inflation, and a weak currency; India, we argued, was not a typical Asian exporter with a strong currency;

- The Fed and US interest rates were the other big risk to India; a failure of successive governments to harness the USD 500 billion of domestic savings into India's capital markets made India excessively reliant on Uncle Ben and his periodic habit of sneezing.

Underpinning all this “worry” and “opportunity” is something real: the movement of hundreds of millions from lower levels of consumption to a higher level of consumption. Unlike the meticulously planned China model or the well-lobbied US model, this movement in India was chaotic and random. A combination of Schumpeter's creative destruction and the randomness of Brownian movement, spiced with Russian-style (or Wall Street style) crony capitalism. Within this chaos, we had to find high integrity managements who would be able to build solid businesses - and buy these liquid stocks at attractive valuations.

Our 100-page presentation on India - and our suggested investment approach - addressed the “Why India?” and “How India?” in detail.

India: Be ready to add a lot

Finance Minister Chidambaram took over charge of the Ministry of Finance on August 1, 2012 and immediately went about his version of reforms: a series of quick-fix speeches. The markets surged and the INR strengthened. Ben Bernanke's QE eternity helped. But the shine has since gone and Uncle Ben's sneeze has given all emerging markets the proverbial cold. Bucked by stubborn inflation and low growth, India has been unloved and unwanted.

Frustratingly, the S&P BSE-30 Index has refused to “collapse” to levels where we would flag the Indian stock markets as an “overweight”. However, as markets puncture individual share prices are coming within our “Buy” limits. Cash levels have decreased - we are seeing more value. The excessively weak INR, in our opinion, will give a further 15% to 20% boost to USD returns. For now - and this may change in a day - we remain with the suggested allocation to India of “50% to 75% of your long term target weight”, a reduction we suggested in September 2012 from our earlier “75% to 100% of your long term target weight”.

But what are the triggers for this cautious optimism?

- The near term looks murky, no doubt, but please do not forget the consumption engine - it may shift from urban to rural India or from premium goods to basic goods, but it's not heading to zero;

- While portfolio investors in India's nascent bond markets may have triggered the recent sell-down in INR on their rapid exit (just as the un-ordained, star-struck P-Note investors exited equity markets in the aftermath of the Lehman bankruptcy) the multinationals want to buy into the India story; reading the annual reports and statements of the multinationals and it is apparent that India is a Top 3 destination for their investment dollars because of the future growth in end demand;

- The Current Account Deficit will head to self-control and near term quarterly data will reflect that; the worry will be oil - a wild card and an unknown; according to a retired CEO of a global oil major who we had the opportunity to meet, the “correct” price for oil is USD 60 to 80 per barrel - everything above that is speculation;

- The fiscal deficit may remain untouched till the next election; in every country there is a pattern of reforms. Changes are made by a newly elected government in the first 12 months of taking office: after that the lobbyists from K Street move in and the surgical extraction of favours commences; India will have an election by May 2014 and history suggests that a patient investor will be rewarded;

- A weak INR and a weak stock market are self-correcting; some magical data point will make every “over-sold” investor cut their bets to “neutral”; we have no clue what that data point is, but we know “sentiment” can turn;

- Earnings growth is still a decent 8% to 10% in the near term and we maintain our 15% to 20% long term nominal growth in earnings; while the overall PER of the market remains unchanged at 16x historical earnings, the capital good sector referred to earlier is now unloved and trades at 1x Price to Book; at the other extreme the Nestle and the Unilever entities in India trade at 40x PER. There is stock-selective opportunity;

Related Post

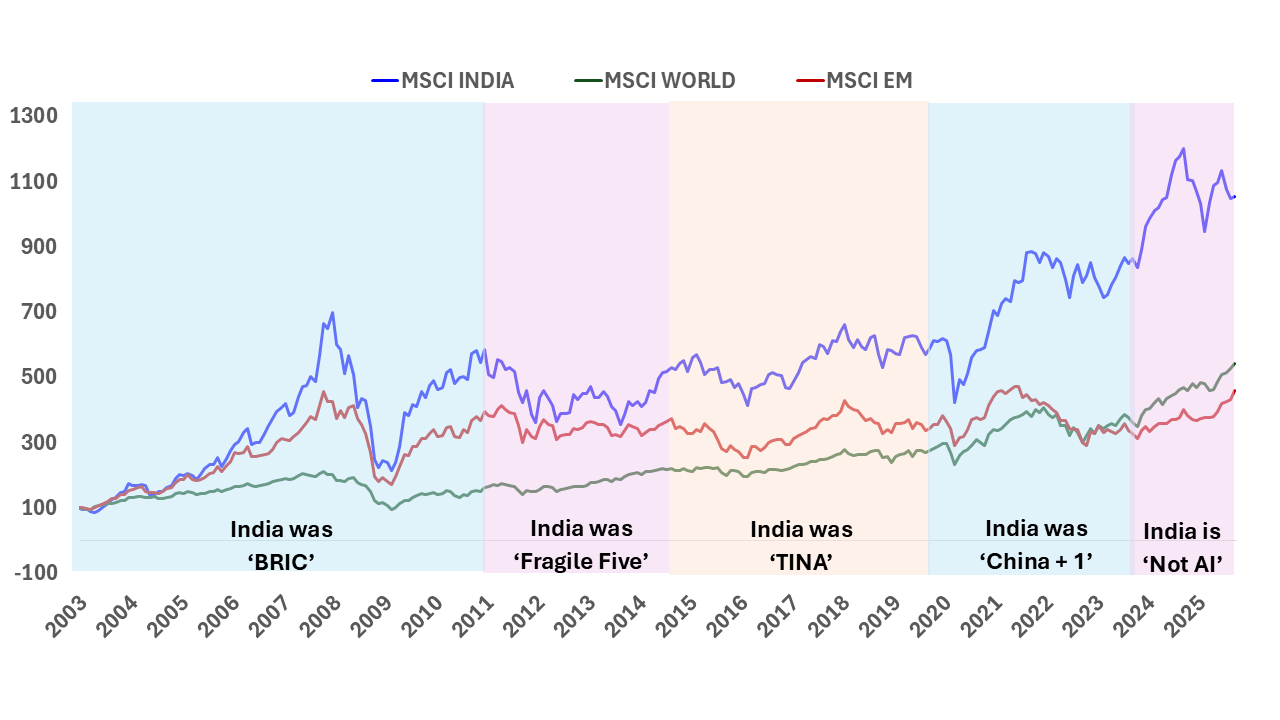

India: T I N A to A N T I

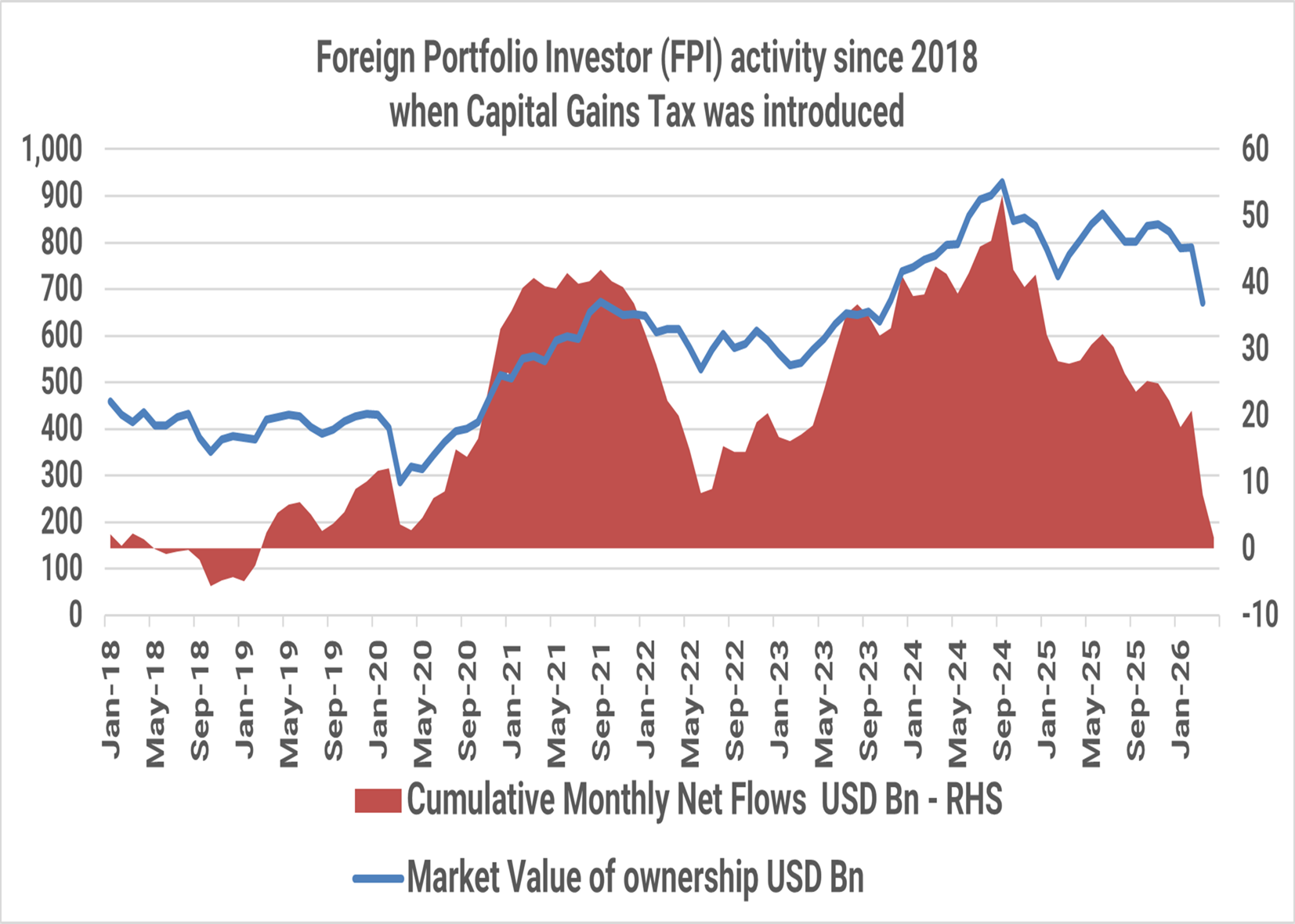

The Indian public equity markets peaked in September 2024. Since then, foreign investors have sold USD 51 billion till April 2026. The market value of foreign investor holding in Indian equities has fallen from USD 930 billion in September 2024 to USD 670 billion, a ~30% drop as at the end of March 2026.

India Investing: From a complicated 2025 to a Simpler 2026?

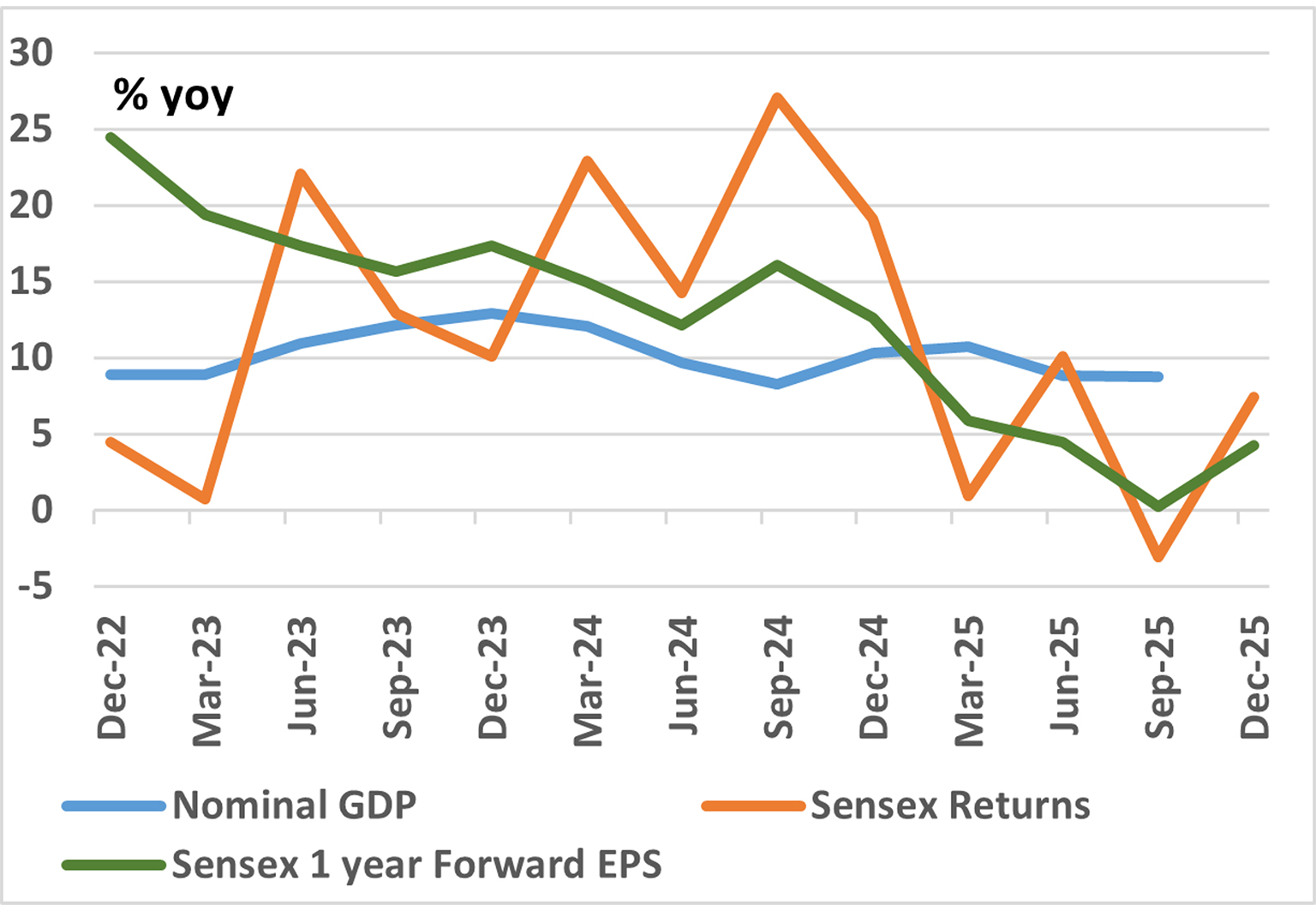

The simple India investing story of double-digit nominal GDP growth reflecting in stock market returns even in dollar terms has faced some headwinds in 2024/2025. Are these headwinds structural? What should investors expect in 2026?

India Investing Under Global Mood Swings

The narrative around global investing is often built around stories. Investors weave these stories around cycles, themes, and opportunities to justify and support their investment rationale.

The Great India Under-Allocation

The most common response to our reach outs to prospective Global Investors to get them interested in Indian Equities is ‘NO’ response.

Our Strategies

Explore how our two main strategies – Predictable India Equity and India Integrity Equity - with demonstrated success of our tried and tested research and investment processes can ensure your India equity allocation will have higher predictable outcomes and no surprises.

Q India Value Equity Strategy

20+ years of India Long-only, Liquid, High-Governance, Margin of safety = Predictability

Integrity screen since 1996, strategy Track record since 2000.

Q India Responsible Returns Strategy

Liquid, proprietary Integrity Scores, Financial Soundness

Integrity Screen since 1996, enhanced criterion since 2015, strategy Track Record since 2019; strategy AuM: $9.7 mn Mandate Capacity: $5 billion

Quantum Advisors pioneered a quantitative as well as qualitative analytical approach to equity investing in India, providing for the first time, consistently applied valuation metrics to evaluate investment opportunities in India’s emerging stock markets. Over the years, Quantum Advisors has continued and enhanced its tradition of extensive financial analysis and value investing, as it has evolved into an investment advisor and asset manager.

Our investment philosophy and strategy involves the use of intensive qualitative and quantitative fundamental analysis. We build and monitor our clients’ portfolios actively while at the same time avoiding excessive trading, and control risk by endeavoring to keep our clients’ portfolio adequately diversified, both in terms of the sectors included in those portfolios, as well as with respect to the level of concentration in any specific security.