Meet the Team: ESG Governance Strategy

Quantum Advisors India

Building your India portfolio since 1990 on a foundation of ethics, integrity & disciplined investment research process.

Nov 30, 2020In this interview Chirag Mehta, Senior Fund Manager (ESG & Alternatives) at Quantum Asset Management talks about his experience of managing the ESG offerings at Quantum. The interview covers the ESG research process, portfolio construction, their experience of ESG engagements with portfolio companies and the steep learning curve.

Chirag Mehta is the fund manager for Quantum India ESG Fund, a mutual fund managed by QAMC. He was ranked as the 4th best Fund Manager in the world under the age of 40 by Citywire in 2017. Chirag is a qualified CAIA (Chartered Alternative Investment Analyst), and has also completed his Masters in Management Studies in Finance.

To learn more about Q India Responsible Returns Strategy, the Quantum Advisors’ ESG offering, please visit our product offerings and one can download fact sheets.

How does Quantum identify companies that meet ESG standards?

The evaluation process consists of a blend of quantitative and qualitative factors.

- Quantitative (30% weight): Companies are evaluated on their levels of disclosures provided in their Sustainability Reports/Business Responsibility Reports/Annual Reports. Companies with higher disclosures get higher scores. For instance, regulations states listed companies should have one Woman on the Board and 50% should be independent, which many companies comply with. As long as they comply, we score them for meeting the regulation. But the spirit of the regulation requires a qualitative analysis.

- Qualitative (70% weight): Evaluate companies on their ESG disclosures and performance – is the Board really independent? Primary research on related party transactions and secondary checks on business practices. We visit factories, meet employees, evaluate vendor’s practices in the supply chain and assess reports from the Pollution Control Boards and NGOs. Also, compare to their peers and national / global regulations on material ESG aspects. Check for any past violations / red flags of certain E&S metrics and corporate governance regulations.

While screening companies, we subjectively evaluate more than 200 parameters across the Environment, Social and Governance domains. While computing the ESG score, 50% weightage is given to the Governance aspect, and the remaining 50% to the Environmental and Social aspects. Governance sits at the heart of our analysis. This is because we believe that it can be a good proxy to understand the company’s E and S performance. We typically focus on areas such as capital allocation, Board composition, quality of disclosures and treatment of minority shareholders.

A positive ESG score, which is a tally of 150-200 parameters of company’s ESG footprints weighted based on materiality to the company’s business, is indeed a measure of long term sustainability of the company. Our proprietary framework to evaluate a company’s ESG practices has evolved into an effective approach to identify companies that are best equipped to handle, and even potentially help resolve, any of current global challenges. It is needless to say that this approach will continue to evolve going further as we aim to perfect the science.

How do you go about constructing the portfolio for the Quantum India ESG Equity Fund?

While we remain market-cap and sector agnostic while constructing the portfolio, we believe in a liquid portfolio. To deliver a ‘transactable’ NAV’, it is important to have stocks that meet our liquidity criteria – we don’t buy stocks that trade a $1 million on an average over the last 12 months.

Quantum’s portfolio construction approach is largely based on the ESG score. Companies with a positive score and are above the minimum threshold ESG score are generally included in the portfolio. Quantum manages to strike a balance by making ESG scores a top priority in capital allocation and adhering to broad sector guardrails to ensure risk mitigation and diversification. Compared to the traditional market-cap based weighted approach, we believe our process is geared to deliver better risk-adjusted returns.

Which sectors/Industries’ do you think are good on the ESG funds parameters and why?

First of all, sectors like alcohol, gambling and tobacco have been in our exclusion list for over 20 years. With ESG, we take a positive approach, looking for businesses that show awareness of material issues and a commitment to sustainability best practices. In a way, this is positive screening for long term sustainable businesses. For instance, while banking per se tend to have lower carbon footprint, if one analyses the carbon footprint of the lending book, it may show a different picture. As disclosures improve, the overall assessment of ESG will also improve.

Many sectors such as FMCG, banking and IT have lower environmental footprint and tend to result in a lop-sided sectoral allocation. However, the importance and contribution of each sector needs to be appreciated. Quantum manages to strike a balance by making ESG scores a top priority in capital allocation as well as adhering to broad sector guardrails to ensure risk mitigation and diversification. We aim to find leaders in each industry that are truly well managed, sustainable, quality businesses. Our analysis is guided by the materiality of the issues and endeavors to build a diversified portfolio of ESG compliant companies which in the long run is expected to outperform conventional market indices.

How has your ESG experience been so far in the real world? Has it delivered to your expectations?

Let me walk through this question in two parts. Firstly – Governance. Quantum adopted what we called an “Integrity Screen” in 1996. If a company/Board does not meet our integrity checks, it will not be included in the portfolio, irrespective of how large the company’s weight is in the benchmark. We have avoided much dubious managements in India over the years. But we have also invested in companies with Governance not at par with the best in the sector but there is a clear intent to improve. We engage with these companies, highlight areas of improvements and most have improved.

Secondly – E & S. While we always had some of the ‘Social’ aspects in-built in our research process (we avoided companies with questionable business practices), we started adopting a formal approach from 2015, in terms of an actual score. We have engaged with our research/portfolio companies on our findings. We have asked for better disclosures, better performance with respect to gender inclusion as well as reducing carbon footprint. Have we changed the world? No. But it has largely been a rewarding experience.

Our ideology and experience of seeing well managed and responsible companies deliver better returns over the long term has translated to an outperformance in the real world. The real world all-encompassing ESG track record of about 16 months indeed looks promising.

Why do you think your proprietary ESG evaluation is superior to ESG indexes?

ESG evaluation requires local knowledge and is not a desk job. Purely relying on company disclosures and controversies to score companies has its downsides. Few benchmark ESG indices are constructed using scores prepared by third-party vendors, which may or may not be robust. In our view, this has resulted in companies with poor corporate governance with high weights in the benchmark indices. We believe that ESG investing needs to be true to label and reflect the underlying ESG characteristics because investors are banking on sustainability to drive the long term performance and not on how big or popular the company is. Importantly from an investment standpoint, once the weight of every stock can potentially change as a result of its ESG characteristics, investors are effectively in the active management space. That’s why actively managed ESG funds continue to attract the lion’s share of dollars and represent a much larger portion of the sustainable investing landscape. We believe this will continue for the foreseeable future.

Can you elaborate on the ESG engagements with companies, with some examples?

We have had mixed results on our engagement efforts. In the initial stages, our engagement focused more on understanding the preparation and oversight of the company’s senior management and Board on key environmental issues. At times we have also engaged with the company when certain disclosures were not forthcoming or the company was in the midst of some controversy.

We engaged with cement companies in our portfolio to understand their long-term targets on emission reduction and what are some of the key challenges to mitigating the environmental impact of their operations. In comparison with global peers, Indian cement companies perform better on parameters such as energy efficiency, water stewardship and use of alternate raw materials to reduce the clinker factor. However, we observed that Indian companies’ use of alternate fuels i.e., the Thermal Substitution Rate (TSR) at 4% was lower than their foreign counterparts which were at ~20%. In addition, we had concerns on the health and safety record of one company and disclosures around water consumption of another company.

Our interaction with the management on the above issues provided us with the insights enumerated below:

- There were a couple of reasons for the low TSR rate. The chief reason for the low TSR was the lack of “polluter pays” principle in force in India and lack of scientific practices of waste management and segregation. Majority of the waste currently used in cement plants is refuse derived fuel (RDF). In India, only 70% of the daily generated municipal waste is collected and nearly 80% is dumped without proper treatment. In developed countries, the generator of waste has to pay a certain price if the waste is disposed in a landfill whereas in India, the waste generator expects to be compensated for selling waste to the cement manufacturers.

- On the health and safety aspect, we realized that the company with a “poor” safety record had a stricter interpretation system in place. They also used to include accidents of the truck drivers who were transporting cement and this led to the safety record being higher than other peers who were providing only plant level data.

- On the water consumption, we asked for the company to provide granular disclosures. Initially we had penalized the company since the water intensity was significantly higher than peers. During our initial interaction with the company, we were made to understand that the high consumption was due to inclusion of water consumption by the housing colonies of the company and the captive power plants. After the company provided better disclosures, we removed the penalty in our rating.

We engaged with an agrochemical company to understand the low female representation in its workforce. The reason provided was that majority of the workforce (70%) comprised people in sales who had to work in remote rural locations and in manufacturing plants. At offices, gender diversity was at ~17%.

One of our portfolio companies refused to provide us key info on E&S. On this occasion, we had to divest from the company. On another occasion, we wanted clarification from an IT company who was a vendor to Boeing. Boeing was under scrutiny for safety lapses in connection with the MAX 737 planes and we wanted to understand the risk faced by the IT Company. On this occasion we had to trim our stake till further clarity emerged on the issue.

Overall, not all companies will engage with us in detail but the trend is slowly improving. Those that are in sectors which are under scrutiny for their large environmental footprint tend to have better disclosures and dedicated teams to handle our queries.

What are the typical issues that investors face when they step in the world of ESG?

In the evolving world of ESG, investors face two critical issues:

- The credibility and depth of ESG research - that really defines the universe

- Sizing of the portfolio /index- Is it reflective of the goodness of ESG investing or is there a conscious effort to mirror the conventional indices to show size?

For many practitioners, ESG scoring comes down to the ability of a company to fill out ESG forms. Given the incentives on green washing, do you only refer to a company’s self-disclosed information or do you seek other types of inputs? A lot of providers rely too heavily on the former, which is a big problem.

We also have some index providers / managers rely solely on third party ESG evaluation of companies to construct an ESG index. In many instances, it is principally down to them missing the point about what is really important for companies from an ESG perspective.

Traditional index construction approaches typically sort a universe of stocks using companies’ ESG scores, eliminating those with the worst rankings, and cap-weighting the remainder. This is due to size, but therein lays the central problem with such indexes: They tend to pick only the largest companies in the world in order to better compare to a conventional index. With traditional ESG approaches, investors need to be aware that ESG bets can be concentrated in certain stocks and duplicate existing market holdings.

How does ESG add value to investment management?

In my view, there are three broad areas where ESG integration adds significant value.

ESG encourages a broader view and allow investors to look beyond their traditional remit

-The impact of E, S, G factors (response to climate change, waste management, fair labor policies, ethical supply chains etc.) on a firm’s long term financial prospects is often underestimated because of their non – financial nature. But like it or not, these tail risks hidden beneath a company’s business activities can have a material impact on the firm’s earnings and valuation over the long term, thus making them important considerations for long term investors. In many ways, it is forward looking.

ESG analysis aims to identify businesses which are well prepared to deal with the emerging complex risks and thus create long term shareholder value

In an increasingly complex and interconnected world, the importance of actively managing risks and opportunities related to emerging environmental and social trends, in combination with rising public expectations for better accountability and corporate governance, presents a new set of challenges with far-reaching financial consequences for corporations in the form of litigation, bad reputation, product boycotts, strikes and factory shutdowns, etc.

And for investors to determine which companies are best equipped to handle and overcome these challenges, it has become essential to evaluate their ESG practices.

Responsibility and profitability are not incompatible, but in fact wholly complementary

There is strong research evidence of ESG investing delivering better returns since companies with strong sustainability scores demonstrate better operational performance and are less risky. Such companies are typically less exposed to tail risks such as environmental accidents or punishment from regulators and excellent ESG standards can function as a guide to a company’s overall quality of management and long-term sustainability.

As millennials age into investors, ESG compliance is here to stay. Since a rising share of a company’s valuation is tied to intangible assets such as brand reputation, environmental and social performance is more material than ever.

How do you navigate the instances of green washing?

We are well aware that there are many “green washing” incentives for companies from brand building to attracting investment flows. And it is our fiduciary duty as custodians of investor capital to navigate any green washing attempts and deliver investors a true sustainability geared portfolio. We understand that ESG is not a “tick the box” desk research. We do not restrict our research to self-declared company disclosures. We try to do a 360 degree company check by talking to various stakeholders like suppliers, vendors, customers, channel checks, employees etc. to get more information to get a granular understanding of the true state of company’s affairs. We also try to get information from unorthodox sources like pollution control boards, NGOs, local communities in our bid to leave no stone unturned. There is also an attempt to verify the information with other available data and mapping with other companies in the sector and globally to identify any red flags.

Analyzing these aspects can be challenging, mostly due to lack of resources. ESG investing is of immense importance and we will help investors navigate the evolving ESG landscape through our proprietary framework based on ground research and years of experience in evaluating companies.

Statutory Disclosure and Disclaimer: Quantum India ESG Fund (“QIESG”) is a fund launched in July 2019 under Quantum Mutual Fund (QMF), an India domiciled public retail mutual fund offered focussing to domestic Indian retail investors. QMF is registered with Securities and Exchange Board of India (SEBI). Quantum Asset Management Company Pvt Ltd (QAMC), 100% subsidiary of Quantum Advisors Pvt. Ltd. (QAPL), is the Investment Manager of QMF.

QAMC provides research/advisory service to QAPL. The information on QIESG is provided for illustration and information purpose only, as QAMC follows a similar investment strategy, process and philosophy for QIESG as that offered by QAPL under Quantum India Equity Governance Strategy. This is neither an offer to sell nor a solicitation of an offer to buy any securities of Quantum India ESG Fund.

We at QAPL receive non-binding and non-discretionary research/advisory services from QAMC with respect to investments by our Private Account clients (including Fund clients). Our evaluation of QAMC’s qualifications, suitability and performance as research/advisory services provider involves inherent conflicts of interest that would not be present if we were instead evaluating independent service provider.

Related Post

India: T I N A to A N T I

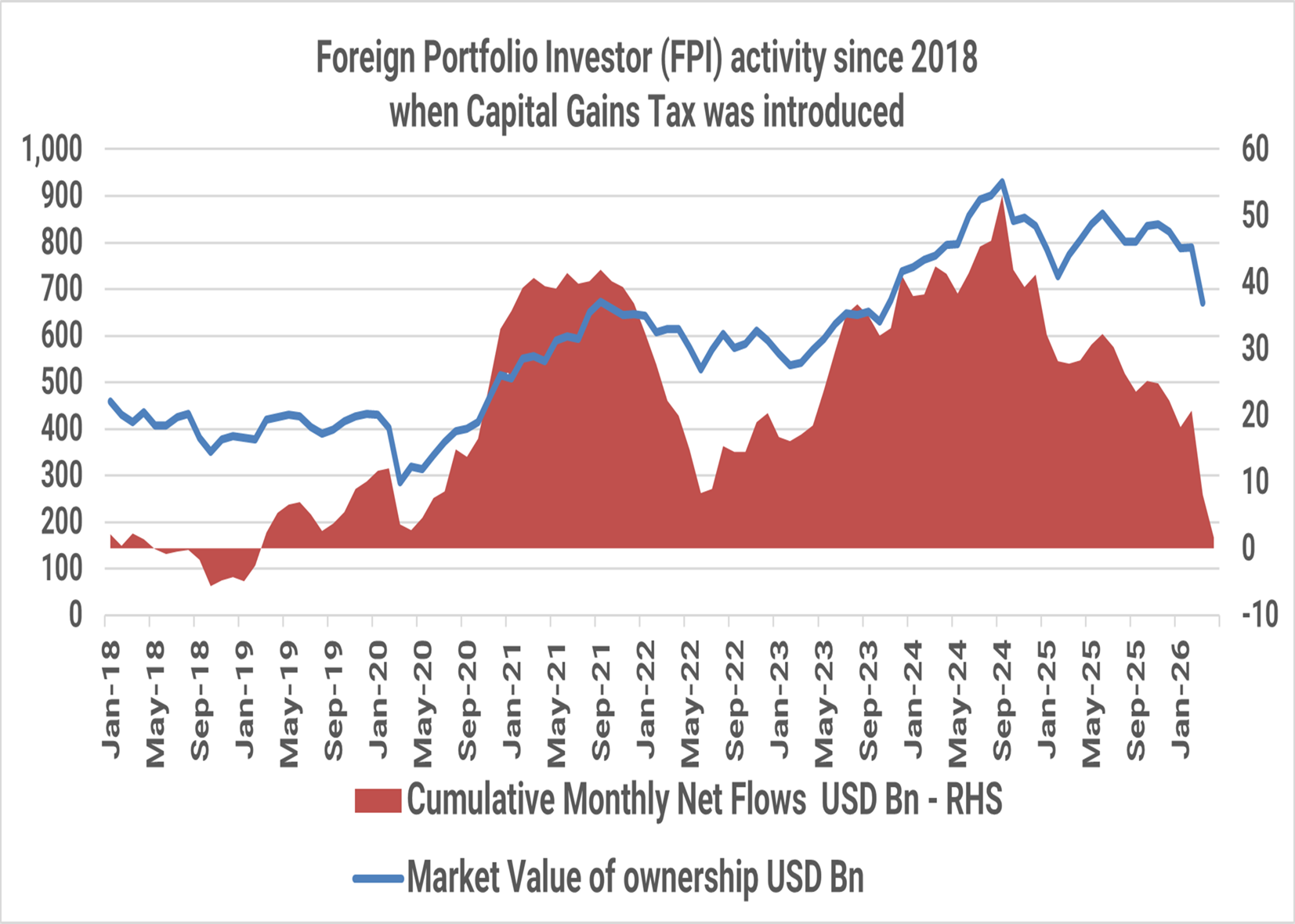

The Indian public equity markets peaked in September 2024. Since then, foreign investors have sold USD 51 billion till April 2026. The market value of foreign investor holding in Indian equities has fallen from USD 930 billion in September 2024 to USD 670 billion, a ~30% drop as at the end of March 2026.

India Investing: From a complicated 2025 to a Simpler 2026?

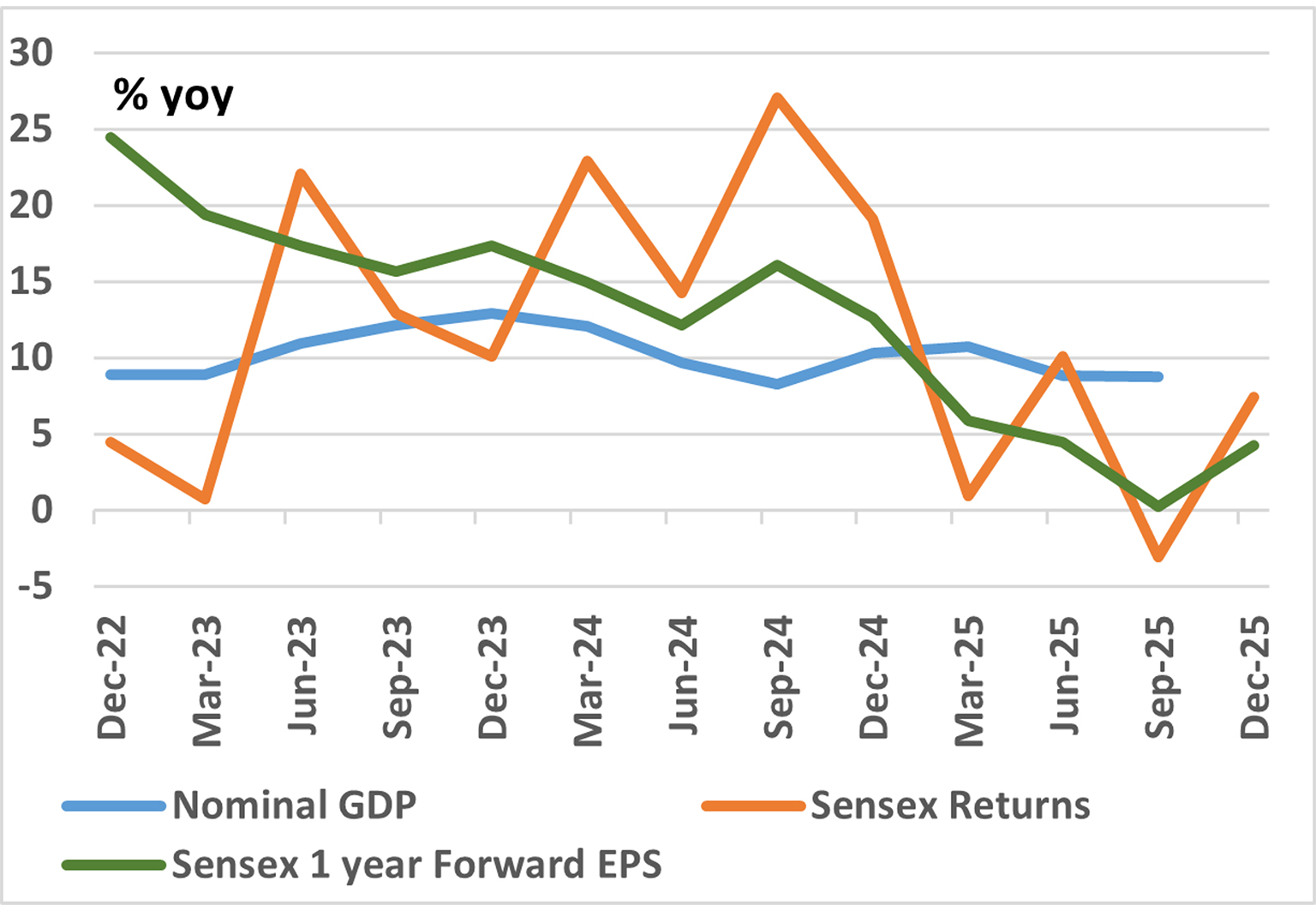

The simple India investing story of double-digit nominal GDP growth reflecting in stock market returns even in dollar terms has faced some headwinds in 2024/2025. Are these headwinds structural? What should investors expect in 2026?

India Investing Under Global Mood Swings

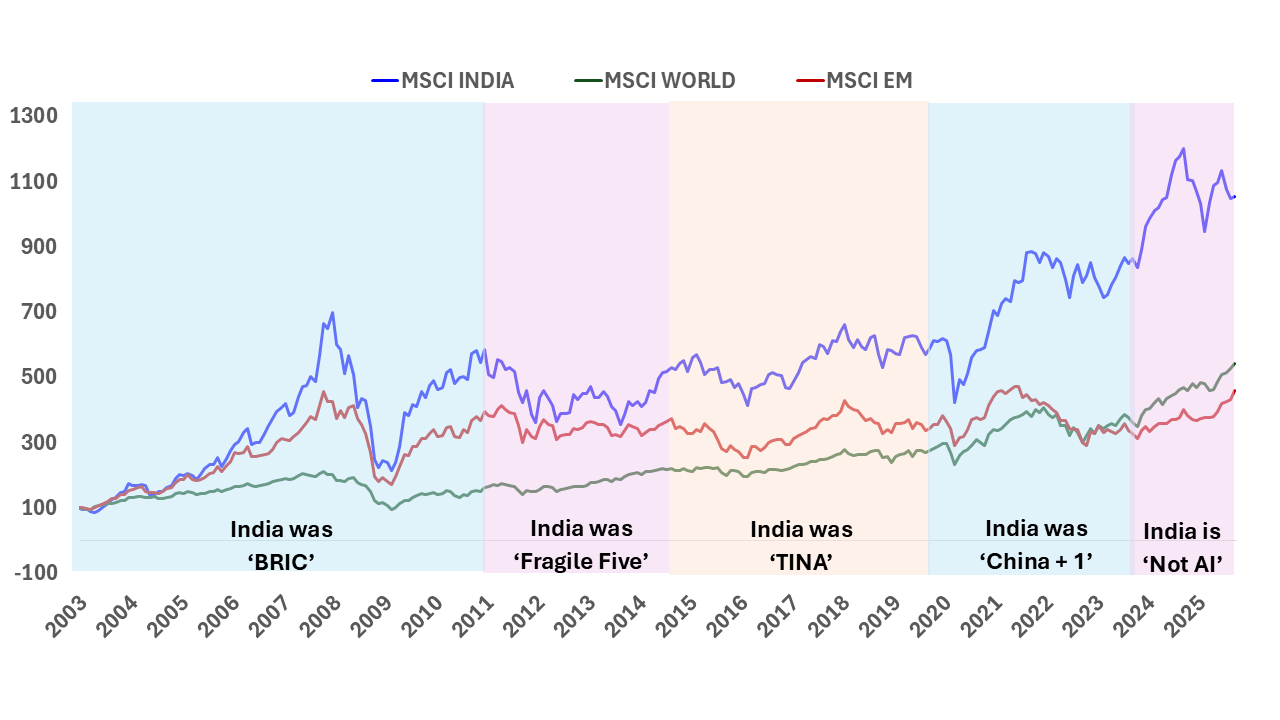

The narrative around global investing is often built around stories. Investors weave these stories around cycles, themes, and opportunities to justify and support their investment rationale.

The Great India Under-Allocation

The most common response to our reach outs to prospective Global Investors to get them interested in Indian Equities is ‘NO’ response.

Our Strategies

Explore how our two main strategies – Predictable India Equity and India Integrity Equity - with demonstrated success of our tried and tested research and investment processes can ensure your India equity allocation will have higher predictable outcomes and no surprises.

Q India Value Equity Strategy

20+ years of India Long-only, Liquid, High-Governance, Margin of safety = Predictability

Integrity screen since 1996, strategy Track record since 2000.

Q India Responsible Returns Strategy

Liquid, proprietary Integrity Scores, Financial Soundness

Integrity Screen since 1996, enhanced criterion since 2015, strategy Track Record since 2019; strategy AuM: $9.7 mn Mandate Capacity: $5 billion

Quantum Advisors pioneered a quantitative as well as qualitative analytical approach to equity investing in India, providing for the first time, consistently applied valuation metrics to evaluate investment opportunities in India’s emerging stock markets. Over the years, Quantum Advisors has continued and enhanced its tradition of extensive financial analysis and value investing, as it has evolved into an investment advisor and asset manager.

Our investment philosophy and strategy involves the use of intensive qualitative and quantitative fundamental analysis. We build and monitor our clients’ portfolios actively while at the same time avoiding excessive trading, and control risk by endeavoring to keep our clients’ portfolio adequately diversified, both in terms of the sectors included in those portfolios, as well as with respect to the level of concentration in any specific security.