Meet the Team: India Value Strategy

Quantum Advisors India

Building your India portfolio since 1990 on a foundation of ethics, integrity & disciplined investment research process.

Dec 17, 2020In this joint interview I. V. Subramaniam or Subbu (Managing Director, CEO & CIO) and Nilesh Shetty (Portfolio Manager) at Quantum Advisors, discuss the bottom-up research and portfolio construction process. The team also shares their experience on how the “Integrity Screen”, adopted in 1996, for evaluating Corporate Governance in India evolved into integrating ESG actively.

Fund Manager Interviews

I.V. Subramaniam “Subbu” has over 25 years of experience in the investment management and financial services industry. Since June 2000, Subbu has managed India-dedicated portfolios for Indian clients and since 2005, he has managed India-dedicated portfolios for international clients. Subbu received his Bachelor’s degree in commerce from Osmania University in 1983 and his Law degree from Osmania University in 1986. He is a CFA Charterholder.

Nilesh Shetty has 16 years of experience in the Indian capital markets as an Analyst and Senior Research Manager. Nilesh joined Quantum AMC in December 2009 and moved to Quantum Advisors in April 2022. In addition to being a portfolio manager, Nilesh is Quantum’s primary analyst for Capital goods, Life insurance, General insurance and Broking. Prior to joining Quantum, Nilesh worked for 2 years at Edelweiss Capital as an analyst. Nilesh received his Masters in Management Studies from Mumbai University in 2003 and is a CFA Charterholder and a Chartered Global Management Accountant having completed CIMA (UK).

Why follow Value Investing in a growth market like India?

Subbu: Over the years, the Indian stock market has had a love/hate relationship with foreign institutional investors. When global risk aversion is low, flows to India significantly increase; we have seen this in 2007, 2010, 2014 and again in 2020 driven by liquidity from global central banks’ easy money policies. In these instances, valuations are no major obstacle as everything is bid up. As soon as risk aversion returns however, investors see the value of their portfolios erode as the fundamentals take precedence and true value is left standing.

India continues to offer great potential with its 1.3 billion-strong consumer market, but government decision making can be erratic, and economic reforms often follow a path of two steps forward and one step back. In the past, investors in India have paid dearly for projecting a goldilocks scenario involving 8%+ GDP growth combined with strong government action. The Indian markets are rife with management teams sporting poor corporate governance track records. So while India is attractive, investors need to guard against these risks and demand an adequate margin of safety. Our long-term track record of delivering 300 basis points of outperformance against the MSCI India Index since inception (31st July 2000) is a testimony to how our investment process can achieve success in the Indian markets while avoiding unnecessary risk.

How does the research process work?

Nilesh Shetty: Our approach to investing is based on principles of long-term value, detailed bottom-up stock research, and an extremely disciplined process. We are value investors, and we believe we are good at identifying high-quality stocks available at a discount to their intrinsic value with an eye towards that discount getting eliminated over time as the stock is valued appropriately.

- We have always been wary of liquidity risk in portfolios. Hence our research process starts with a liquidity filter. Each stock one of our analysts tracks needs to have an average daily trading volume of USD 1 million over the last 1 year for it be considered to be a part of research coverage.

- The valuation models we use vary by sector. We have used Price-to-Earnings ratios, Price-to-Book ratios, Price-to-Sales, EV/EBITDA, EV/tonne, discounted cash flow, and sum of parts as valuation measures. The valuation of a company is based on a normalized assumption of the business environment free from any cyclicality or abnormality. We normally use the 2-year forward earnings estimate for valuing a company, and earnings multiples are set based on the valuation band in which a stock has traded in the past.

- Since the portfolio follows a value style, our research reports tend to factor most of the negative news and analyst numbers have scope for upside. When uncertainty levels are high, our analyst reports include a sensitivity analysis of how projections would change based on various scenarios.

- While valuing a company, we generally give a 40% discount to intrinsic value in setting our buy price. However, that discount varies across sectors depending on the inherent risks we foresee. For example, we are comfortable with a lower discount of 30% in consumer staples, as economic cycles have relatively less impact on the earnings growth of the companies. We ask for a 40%-50% discount to intrinsic value in the case of real estate companies, as earnings volatility tends to be much higher for these companies due to their cyclicality. This gives us a margin of safety for any errors or omissions in our assumptions.

- Our analyst assumptions are discussed at length by the entire research team before being approved unanimously in order to ensure all relevant variables are factored in our assumptions.

- Each stock approved by the research team has a pre-assigned Buy/Sell Price. The data of each stock is maintained in an ‘Estimates Database’.

- We maintain 100% of the equity universe under active coverage in house.

- Given our focus on corporate governance, we have avoided investment in companies:

- With a record of treating minority shareholders poorly

- That have blatantly violated environmental rules and regulations

- That have acquired national properties from the government through questionable means

- With questionable accounting practices

- With weak business models

- Where it is not clear as to who exactly the founders of the company are

- That follow other similarly questionable practices as those enumerated above

How does portfolio construction work?

Nilesh Shetty: Our goal is to build a diversified portfolio of 25-40 stocks which can generate a reasonable risk-adjusted return. Once the research team determines the buy and sell prices of a stock, the portfolio team – which is also part of the research team – does not second guess it. The portfolio team then uses those pre-determined prices to guide decision making. It is not uncommon for us to add to a stock we already own in between the Buy and Sell prices. We will generally trim the position’s weight when our calculated upside potential falls below that of the India long bond return. Individual stock weights are determined as a function of:

- Reliability of management

- Quality of earnings

- Stability of earnings

- Upside potential

- Alternatives/cash

The first three points are afforded the highest importance. For instance, if we are deciding between two stocks with similar upside potential, the one that scores higher on the first three metrics will earn a larger weight. Within this framework, stocks are added at a minimum weight of 2% and a maximum of 6% at cost. On a market value basis, we allow stocks to move up to a maximum of 10% weight and then trim it. Our research is updated at least every 180 days by the covering analyst.

We sell when the stock price reaches our sell limit and there has been no revision in our sell limits, or when we change our view on the management.

Cash is a residual of the portfolio process; we do not take an active call on it. If we do not find new opportunities in which to invest and elect not to add to existing company positions, we are content to hold the cash. Our average cash level since inception is 11.4%. Ideally, we prefer not to have any client restrictions in holding cash, but specific clients do have mandates restricting that weight. In our restriction-free portfolio, the highest cash level we have held was 30% in 2015.

What makes Quantum Advisors unique in India?

Subbu: There are very few India managers with a history as long as ours. There are even fewer India managers who follow a disciplined value style and can back it up with a track record to match. We believe our focus on a combination of liquidity, corporate governance, valuation, in-house research and a focus on the long term remains unique to the investment landscape in India. We have seen investors suffer heavy losses when they ignore one of the above criteria in India. While it may work in the short term when risk aversion is low, it has tended to inflict significant permanent impairment of capital when risk aversion increases.

In general, our competitive position and strength rests on the following pillars:

- A rigorous, team consensus-style research process

- A long-term perspective: investing patiently for patient capital

- Proprietary research – not dependent on external sources

- Our belief that it is important to have a macro view on India for the long term, as this is the framework under which the investee companies will operate. The key is to focus on management teams’ capacity to guide their businesses across different economic and social environments while at the same time respecting minority shareholders and the rule of law.

In addition to all of the above, our competitive advantage is enhanced by our strong focus on risk assessment before making investments.

How does the strategy perform under different market environments?

Subbu: Given our value investment style, our investment performance tends to mirror how traditional value strategies perform across market scenarios.

- Bull Markets: In bull markets, our strategy is likely to underperform as we sell the stocks that have hit our sell limits and find limited opportunities to redeploy our cash. As bull markets may favor growth names, our value strategy has a propensity to underperform. This held true in 2006, 2007, and 2019 under similar conditions.

- Bear Markets: In bear markets, our strategy is likely to outperform the broader markets as the kind of value stocks we hold tend to fall less relative to other stocks. This held true in the bear markets of 2008 and 2015.

- Flat Trendless Markets: Our portfolio performance is likely to outperform the markets due to superior stock selection.

- High Volatility Markets: In a volatile market, our strategy is likely to outperform the market as we get opportunities to sell the stocks that hit our sell limit while also affording us the opportunity to buy those and other stocks that decline to our buy limit. We outperformed in 2008 and 2020 in similar conditions.

- Low Volatility Markets: Our portfolio performance is likely to underperform if, as is typical, the low volatility is a result of upward trending markets.

We believe that over a complete cycle the style will outperform, but there will be periods of euphoria or irrational exuberance in between in which we are likely to underperform.

How is ESG integrated in your value portfolio?

Nilesh Shetty: As part of our normal research process, we have always given primary emphasis to corporate governance factors and have excluded those companies that have demonstrated a poor governance track record. From 2015 onwards, based on the increasing importance of non-financial factors (Environment and Social) as well as regulations mandating disclosures on ESG metrics, we developed a proprietary methodology to formally rate companies in our investment universe on these ‘E’, ‘S’, and ‘G’ metrics. We have a six-member team dedicated to ESG research in determining these scores.

Generally, the ESG rating does not serve as the sole determining factor in the decision to include or exclude companies in our portfolio. However, when we observe any portfolio company involved in serious violations of ESG practices and management or the Board demonstrates no intent to improve, the portfolio team will divest the company. For non-portfolio companies, the stock will be placed on “Permanent Watch” and will not be bought – irrespective of market price – until our concerns have been satisfactorily resolved.

Can you give an example of ESG factors determining a portfolio action?

Nilesh Shetty: We had several issues with a large Engineering & Construction company which was executing an ecologically-sensitive project without doing any internal studies on the environmental risk involved. (Over and above that, it was accused of facilitating bribes on behalf of one of its clients in seeking permits, as confessed by said client – a US-listed company – in a disclosure to the US Securities and Exchange Commission.)

We wrote the board and sought a meeting with the CEO. In the meeting we were told that with respect to the construction project, the environmental risk assessment remained the client’s responsibility and that it would not conduct said assessment itself. With respect to the bribery allegations, the CEO told us there was no incriminating evidence found in emails or invoices with regards to those projects.

The portfolio team decided to exit the position in April 2019 due to A) a lack of serious effort to uncover any individuals involved in facilitating bribes, and B) the risk that the company may be exposed to large penalties in the future, due to the environmental consequences of ecologically-sensitive projects like the coastal road.

Related Post

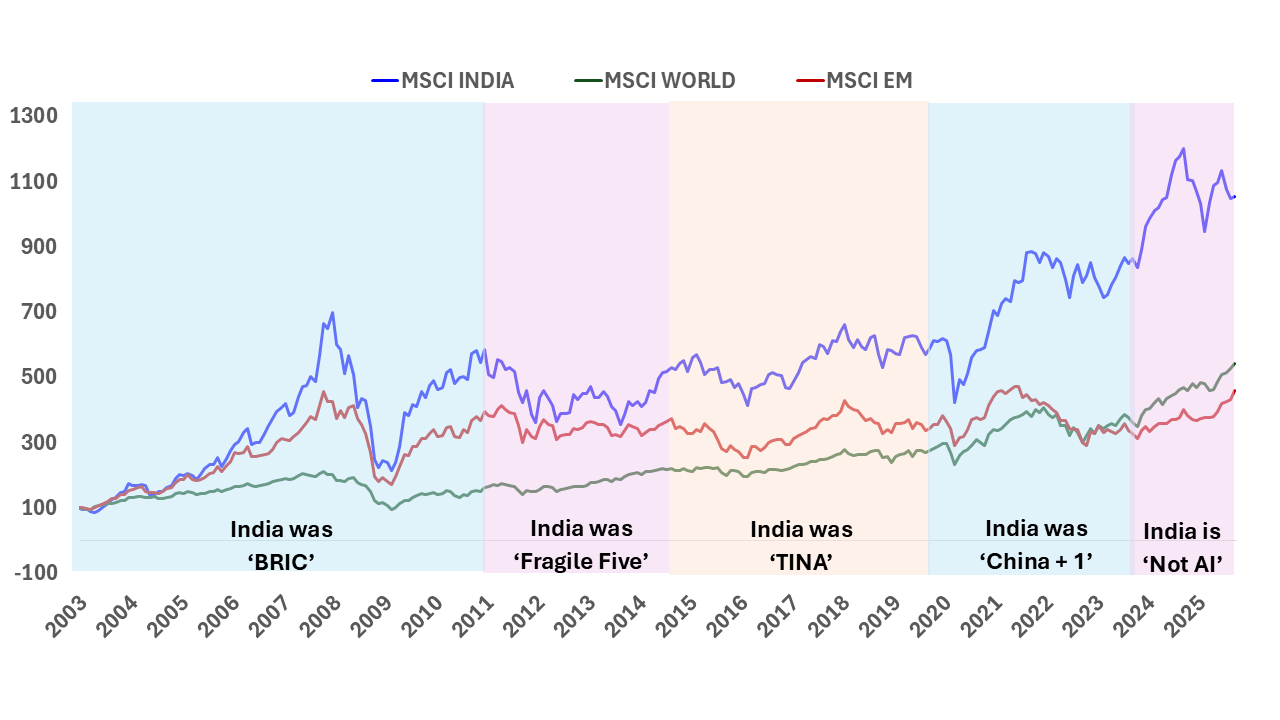

India: T I N A to A N T I

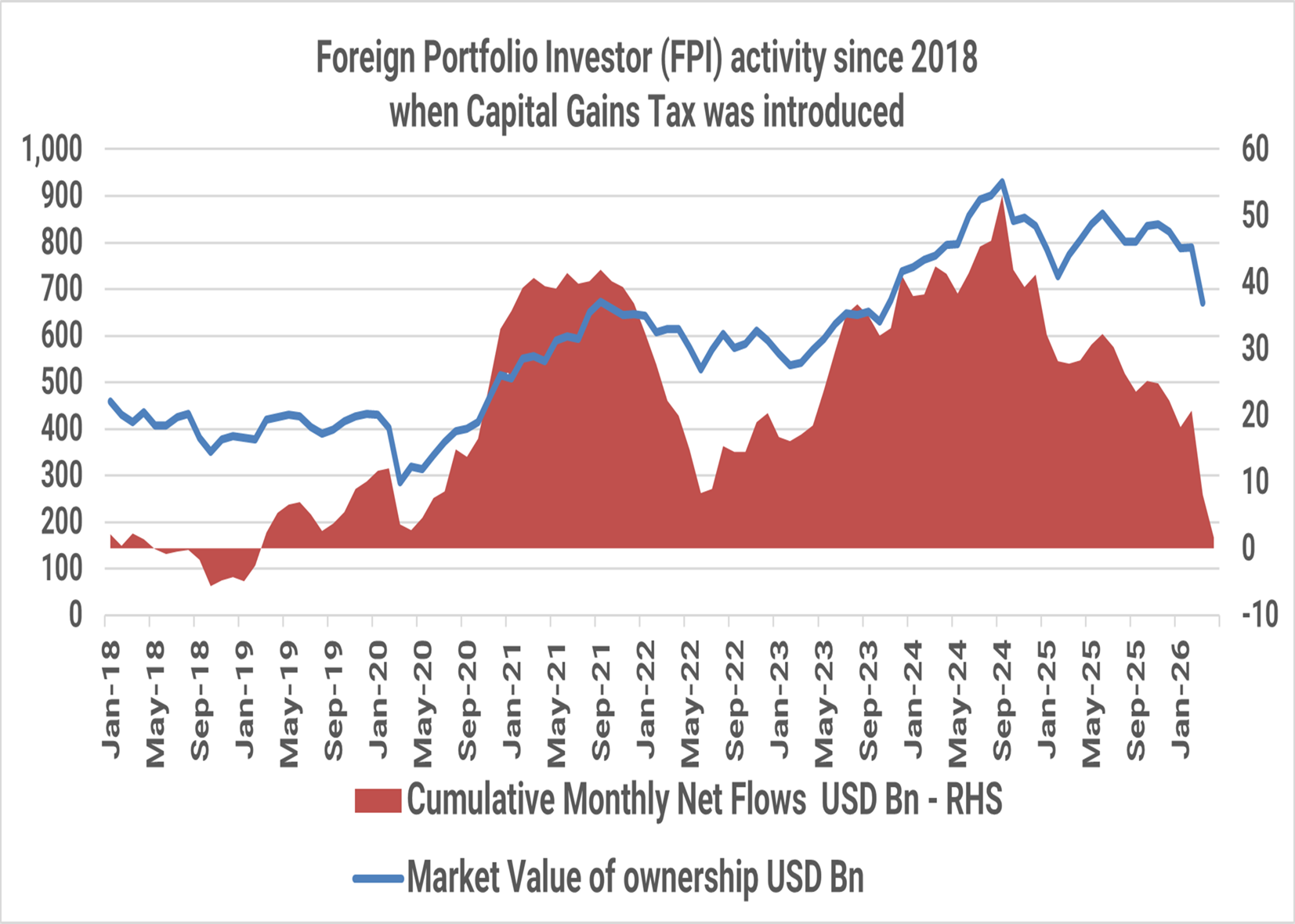

The Indian public equity markets peaked in September 2024. Since then, foreign investors have sold USD 51 billion till April 2026. The market value of foreign investor holding in Indian equities has fallen from USD 930 billion in September 2024 to USD 670 billion, a ~30% drop as at the end of March 2026.

India Investing: From a complicated 2025 to a Simpler 2026?

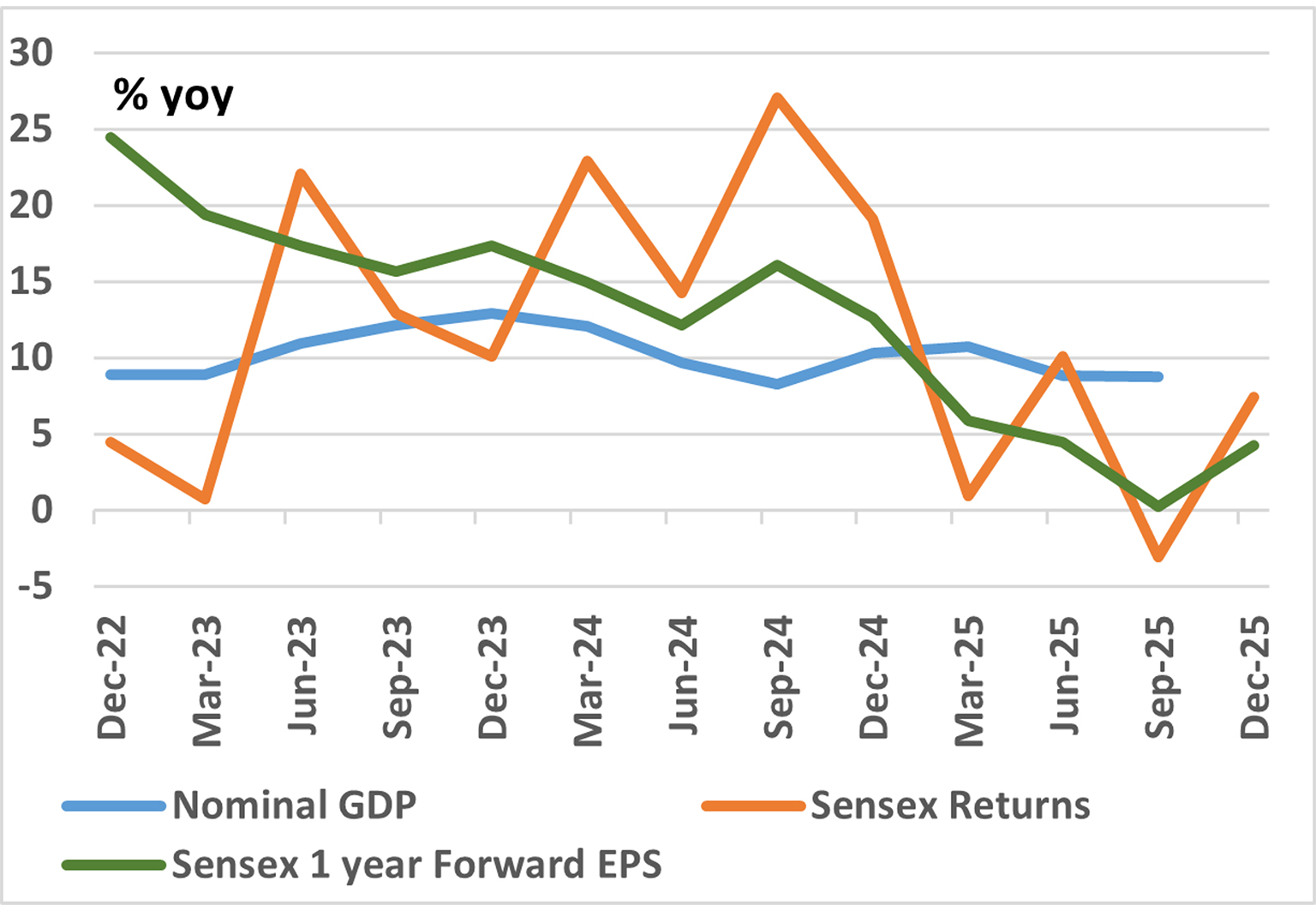

The simple India investing story of double-digit nominal GDP growth reflecting in stock market returns even in dollar terms has faced some headwinds in 2024/2025. Are these headwinds structural? What should investors expect in 2026?

India Investing Under Global Mood Swings

The narrative around global investing is often built around stories. Investors weave these stories around cycles, themes, and opportunities to justify and support their investment rationale.

The Great India Under-Allocation

The most common response to our reach outs to prospective Global Investors to get them interested in Indian Equities is ‘NO’ response.

Our Strategies

Explore how our two main strategies – Predictable India Equity and India Integrity Equity - with demonstrated success of our tried and tested research and investment processes can ensure your India equity allocation will have higher predictable outcomes and no surprises.

Q India Value Equity Strategy

20+ years of India Long-only, Liquid, High-Governance, Margin of safety = Predictability

Integrity screen since 1996, strategy Track record since 2000.

Q India Responsible Returns Strategy

Liquid, proprietary Integrity Scores, Financial Soundness

Integrity Screen since 1996, enhanced criterion since 2015, strategy Track Record since 2019; strategy AuM: $9.7 mn Mandate Capacity: $5 billion

Quantum Advisors pioneered a quantitative as well as qualitative analytical approach to equity investing in India, providing for the first time, consistently applied valuation metrics to evaluate investment opportunities in India’s emerging stock markets. Over the years, Quantum Advisors has continued and enhanced its tradition of extensive financial analysis and value investing, as it has evolved into an investment advisor and asset manager.

Our investment philosophy and strategy involves the use of intensive qualitative and quantitative fundamental analysis. We build and monitor our clients’ portfolios actively while at the same time avoiding excessive trading, and control risk by endeavoring to keep our clients’ portfolio adequately diversified, both in terms of the sectors included in those portfolios, as well as with respect to the level of concentration in any specific security.