Quantum Advisors India

Building your India portfolio since 1990 on a foundation of ethics, integrity & disciplined investment research process.

The split in the Monetary Policy Committee (MPC) voting in the August 2021 meeting from 6-0 to 5-1 on the stance of the monetary policy and the relative confidence in the RBI to announce higher Variable Rate Reverse Repo Auction (VRRR) auctions to suck out liquidity suggests that thinking within the RBI on normalising monetary policy has begun.

Over the next six months, we would expect RBI to reduce the excess liquidity in the banking system; we would expect an increase in the reverse repo rate from 3.35% to 3.75%; a subtle move away from the accommodative stance to neutral and then later on to a gradual beginning of rate hikes to narrow the gap between the short term interest rates, currently below 4%, and current inflation of around 5.5%.

This sequence of monetary policy normalisation is now almost consensus. Certain segments of the bond markets have already priced in some of the near-term impact of these forthcoming actions.

However, markets remain unsure on the timing and the extent to which the RBI will normalise. In trying to answer that question, a more fundamental question must be asked and answered – What is normal?

What is Normal?

Before we begin asking and answering that question, it is always instructive to look at long term data.

Averages for real GDP growth, consumer price index inflation, the repo rate, fiscal deficit and bond yields are given below.

Data only till March 2020 has been taken. This, as the pandemic resulted in FY 21 being an unusual year. As we look out for normalised times ahead, policy makers will look for data trends in a normal situation.

| All Data up to March 2020 | 20 year Average | 10 Year Average | 5 Year Average |

|---|---|---|---|

| Real GDP % yoy | 7.03% | 6.97% | 6.73% |

| CPI % yoy | 6.22% | 6.44% | 4.13% |

| Repo Rate % | 6.88% | 6.82% | 5.89% |

| 10 Year Bond Yield % | 7.58% | 7.66% | 6.95% |

| Combined Fiscal Deficit % of GDP | 7.26% | 6.71% | 6.40% |

(Source: CMIE, RBI) (current Repo Rate is 4%; the 10 year bond yield is at ~6.2%; the CPI is expected to average 5.5%.; combined fiscal deficit will be ~9.5% of GDP)

As the table above shows, despite the claims of structural changes in the Indian economy, macro indicators have remained in a tight range. The level of current interest rates, however, is a distance away from long-term averages -- one reason why we talk about normalisation.

But the determination of what path that normalisation will take depends on the view taken by policymakers on growth, inflation and the extent of fiscal accommodation.

What is India’s Normal GDP Growth Going Forward?

The first question to ask and answer is around growth. Can India grow at the 7% real GDP rate it averaged in the last 20 years? Has that growth trend dropped to 6% (below its 40 year average)? Or have the multiple shocks in the last 5 years taken the potential real GDP growth to even below 6% as opined by a few economists?

The answer to this question will determine the conduct of RBI’s monetary policy going forward.

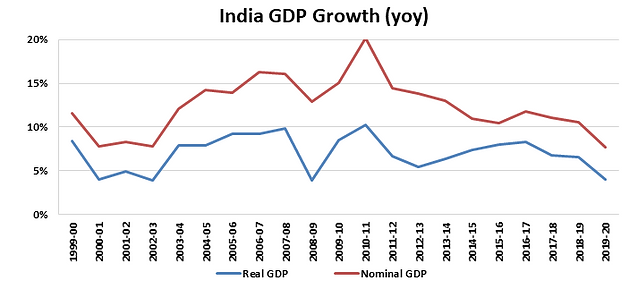

Chart 1: Can India real GDP grow at 5%, 6% or 7%?

Line chart of India’s GDP growth (1999–2020) showing nominal growth consistently above real growth, both peaking around 2010–11 and gradually moderating thereafter.

Source:

During the period of the BRICs mania, India was expected to grow forever in double digits. The government and the RBI also believed in the high growth expectation and chased that through fiscal and monetary policies post the Great Financial crisis of 2008. We know how that flight of fancy ended.

Today, given the slowdown in the four years leading to the pandemic, many are even doubting India’s 6% long-term GDP growth potential.

At Quantum we have long held that India’s long-term GDP potential is 6.0%-6.5%. The government’s decision to keep fiscal deficit at 4.5% till FY 2026 should allow for growth to durably recover to those levels.

The way to think about interest rates relevant for the economy is to determine it on the level of output growth desired. The normal understanding is that as the GDP growth rises, interest rates also rise to ensure that the economy does not get over-heated.

Put another way, higher growth potential can also tolerate a higher relative interest rate. This is in line with India’s history as shown in the first table. India has managed to grow at 6.5%-7.0% with interest rates around 7% and CPI around 6.0%-6.5%

However, in today’s scenario, the Indian economy recovering from pre and post pandemic shocks, does require the support of low interest rates to boost credit, investments and hence consumption.

If the RBI believes that India can grow at 7%, and the economy needs time to reach that level, it will be far more tolerant of inflation and try and keep interest rates as low for as long as possible. This line of thinking will delay the normalisation process and impact the extent of normalisation.

If the RBI believes that India’s potential GDP growth is 5%, we would think they would have more certainty on it being achieved and also contend that excessive pump-priming will only lead to higher inflation. This should ideally lead them to move away from the accommodative stance and push up interest rates faster to manage any inflationary pressures. However, the level of interest rates required will be lower than earlier.

Thus, both these scenarios point to RBI trying to hold rates at a lower level than normal.

If higher growth is to be achieved, interest rates need to be lower.

If the potential growth has fallen, then the economy will operate at lower interest rates.

The current RBI policy stance, liquidity management and interest rates seem to be set up more towards trying to achieve the 7% GDP growth rate. Many aspects suggest that to be the case.

Tolerating Higher Inflation to Secure Growth

While the focus remains on growth for now, it must be kept in mind that India now operates under a flexible inflation target of 4 (+/-2)%.

Would that lead to quicker normalisation as retail inflation remains elevated at least compared to the mid-point of that target? It may not.

From recent commentary, it seems that inflation targeting has moved to CPI being in a band in between 2% - 6%; as against 4% being the mid-point target. Dr. Patra, the Dy.Governor, RBI mentioned in the post policy press conference, that RBI does not want any output sacrifice by responding to the higher inflation through higher interest rates.

Instead, the central bank will prefer to disinflate over a period of two-three years to minimise the output sacrifice, Patra said.

This suggests that normalisation of rates will indeed be driven by growth and what the RBI sees as potential growth.

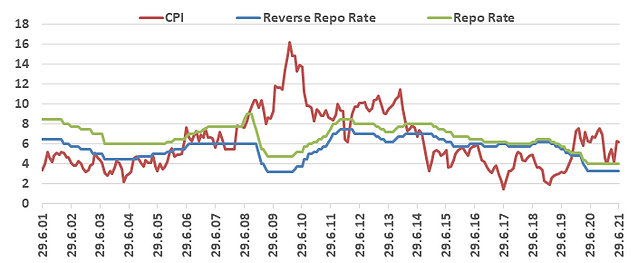

Chart 2: Can Indian Policy rates be normalized below its long-term averages?

(Source: RBI, MOSPI)

Supporting and Bankrolling Fiscal Spending

The fact that the union government has outlined a wider fiscal deficit going out 5 years upto 2026 should give some comfort to the RBI on the growth recovery. The economy will have fiscal support of ~8% of GDP on average over the next 5 years, higher than historical average.

India’s history though suggests a period of high deficits leads to high inflation and subsequently a weakening currency. Although, the global world now seems more forgiving of high deficits, but an emerging market country like India can quickly lose credibility if the high deficits lead to high inflation.

The RBI, given that it isn’t focusing on the 4% CPI target, has borrowed some leeway out of a deficit fueled inflation. They have also taken comfort on government spending being more capex than revenue. Also, for now they seem to have placed a rather high trust on the ability of this government to yet again control food prices and hence the overall CPI inflation.

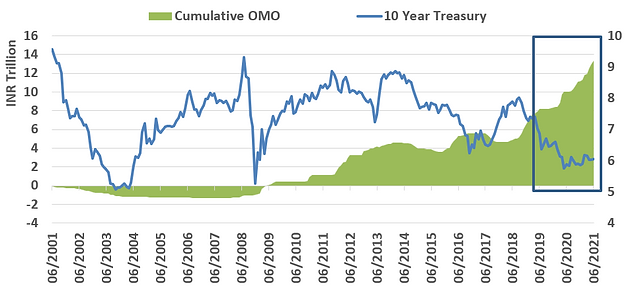

Under Das, this RBI has also become more zealous in its role as a debt manager. They may be cognizant of the inflation risks of higher deficits, however they seem to be more sensitive on ensuring a lower cost for the government borrowing.

The ‘orderly yield curve being a public good’ is also indicative of the fact that even when policy rates eventually rise, the RBI will continue its market interventions and keep a firm control on the government bond yields.

Chart 3: Das unleashes India’s QE to control bond yields

Chart showing cumulative RBI OMO purchases rising sharply after 2019 while 10-year treasury yields decline toward ~6%, highlighting increased liquidity alongside falling yields.

(Source: RBI, OMO= open market operations, Government bond purchases by RBI, QE=Quantitative Easing)

All Signs Thus Point to a Lower ‘Normal’

A final fact to consider is that the RBI and MPC do not even talk about real interest rates anymore. This suggests that India will continue to have low or negative real interest rates. India’s large Asian neighbours, China and Indonesia, also hit by the same pandemic, have managed to keep short term real interest rates positive despite the growth challenge.

This does not bode well for India’s intention to attract foreign money in the bond markets. For now though, given the excess capital inflows into the Equity markets, RBI will weigh its policy balance favouring equity investors over debt and keep real rates low or negative.

This is a big change from the previous regime. The RBI can now potentially hold its policy rate at or below the level of inflation.

We estimate India’s long-term CPI inflation in the 5.0%-5.5% range. If that be so, the RBI can try and hold the Repo rate at say 5.0% to achieve its growth objective.

As we look out over the next year, we do see rates higher as mentioned. However, we think the RBI will be slow to act and try and indicate to the markets that a policy rate of 5.0% in itself may be the ‘new normal’.

Of course, it all depends on global commodity prices and India’s fiscal spending policies, to see if growth can sustain above 6% and inflation can remain in the 5.0%-5.5%.

However, it so seems, we may have to ignore the weight of historical long-term averages and adapt to a scenario of Indian rates trying to be held at a lower level than usual.

Will this growth supportive monetary and fiscal stance take us back to a time when Governor Subbarao had to face the wrath of the global financial markets as inflation soared?

Back then, the RBI response to a challenging inflation, foreign exchange scenario was slow. However within a year of the start of the normalisation, the RBI had hiked rates by 300 bps by March 2011 and despite that India made it to the ‘fragile five’ list in 2013.

Das, who is sure to continue for another two years as Governor, would hope and pray that global conditions remain benign to allow him to operate Indian rates in a ‘new normal’.

In a following piece, we will look at what would it mean for bond markets and for fixed income investments, if Indian rates indeed are held at a lower level than normal.

For more information and if you wish to discuss the details in the article or if you wish to know more about our investment strategies, the investment philosophy and investment opportunities, please contact:

Arvind Chari – [email protected]

https://www.qasl.com/insights/categories/india-macro

Arvind Chari is the Chief Investment Officer (CIO) at Quantum Advisors. Arvind’s vast experience in managing money for global investors and his interactions with leading institutions has exposed him to a world of knowledge. With over 18 years of experience in tracking domestic and global economy he is Quantum’s thought leader and is the author of this Q-India Insight edition.

Important Disclosures & Disclaimers:

1. Quantum Advisors Private Limited (QAPL) is registered in India and holds a Portfolio Management License from Securities and Exchange Board of India (SEBI), India. It is also registered with the Securities Exchange Commission, USA as an Investment Adviser and a Restricted Portfolio Manager in the Canadian Provinces of British Columbia (BCSC), Ontario (OSC), and Quebec (AMF). It is currently not registered with any other regulator. Registration with above regulators does not imply any level of skill or training

2. This summary is subject to a more complete description and does not contain all of the information necessary to make an investment decision, including, but not limited to, the risks, fee and investment strategies of QAPL.

3. This article is strictly for information purposes only and should not be considered as an offer to sell, or solicitation of an offer to buy interests in the account. Investments in the equity and fixed income instruments are not guaranteed or insured and are subject to investments risks, including the possible loss of the principal amount invested. The value of the securities and the income from them may fall as well as rise. Past performance does not guarantee future results and future performance may be lower or higher than the data quoted, including the possibility of the loss. Quantum Advisors reserves the right to make the changes and corrections to its opinions expressed in the document at any time, without notice. Information sourced from third parties cannot be guaranteed or was not independently verified. Comments made herein are not necessarily indicative of future or likely performance of the account and are based on information and developments as at 10/08/2021 unless otherwise stated.

4. All of the forward-looking statements made in this communication are inherently uncertain and Quantum Advisors (QAPL) cannot assure the reader that the results or developments anticipated by QAPL will be realized or even if realized, will have the expected consequences to or effects on, us or our business prospects, financial condition or results of operations. A prospective investor can generally identify forward-looking statements as statements containing the words “will,” “should”, “can”, “may”, “believe,” “expect,” “anticipate,” “intend,” “contemplate,” “estimate,” “assume”, “target”, “targeted” or other similar expressions. Readers are cautioned not to place undue reliance on these forward-looking statements in making any investment decision. Forward-looking statements made in this communication apply only as of the date of this communication. While we may elect to update forward-looking statements from time to time, we specifically disclaim any obligation to do so, even if internal estimates change, unless otherwise required by applicable Securities law

UK related important disclosures

The protections conferred by or under the Financial Services and Markets Act (FSMA) will not apply to this newsletter and any ESG based investment activity undertaken by us.

The protections conferred by or under the FSMA may not apply to any investment activity that may be engaged in as a result of this newsletter.

The applicability of any dispute resolution scheme or compensation scheme and its jurisdiction (if and where applicable) pertaining to a transaction resulting from this newsletter would be as specified in the respective client agreements.

Our History

Quantum Advisors was founded by Ajit Dayal as India’s first institutional equity research house in January 1990.

Our Strategies

Explore how our two main strategies – Predictable India Equity and India Integrity Equity - with demonstrated success of our tried and tested research and investment processes can ensure your India equity allocation will have higher predictable outcomes and no surprises.

Q India Value Equity Strategy

20+ years of India Long-only, Liquid, High-Governance, Margin of safety = Predictability

Integrity screen since 1996, strategy Track record since 2000.

Q India Responsible Returns Strategy

Liquid, proprietary Integrity Scores, Financial Soundness

Integrity Screen since 1996, enhanced criterion since 2015, strategy Track Record since 2019; strategy AuM: $9.7 mn Mandate Capacity: $5 billion

Quantum Advisors pioneered a quantitative as well as qualitative analytical approach to equity investing in India, providing for the first time, consistently applied valuation metrics to evaluate investment opportunities in India’s emerging stock markets. Over the years, Quantum Advisors has continued and enhanced its tradition of extensive financial analysis and value investing, as it has evolved into an investment advisor and asset manager.

Our investment philosophy and strategy involves the use of intensive qualitative and quantitative fundamental analysis. We build and monitor our clients’ portfolios actively while at the same time avoiding excessive trading, and control risk by endeavoring to keep our clients’ portfolio adequately diversified, both in terms of the sectors included in those portfolios, as well as with respect to the level of concentration in any specific security.