Why Adani demonstrates the G should come first in ESG... at least in India

Quantum Advisors India

Building your India portfolio since 1990 on a foundation of ethics, integrity & disciplined investment research process.

July 2, 2024Adani is almost an anagram of India, but not quite. In the embattled Group's response to Hindenberg's explosive research report, which derailed their $2.4bn fund raising, the company's 413 page rejoinder included the phrase, 'this is not merely an unwarranted attack on any specific company but a calculated attack on India, the independence, integrity and quality of Indian Institutions , and the growth and ambition of India.'

In reality, there are many specific aspects of the Adani situation that are mirrored in multiple other corporate governance scandals that have emerged all over the World in recent decades, while others arise more specifically from India's particular model of economic and political development. Navigating all of these aspects carefully is required to manage risk and avoid damaging 'potholes' while participating in the economic expansion of the World's fastest growing and demographically advantaged large economy.

Surprising to Many Who Track India

What is a surprise to many who track India is that the Adani episode seems to have come as such a surprise. Like similar situations, the only unknowns were: when? how? who? The 'why' is a given for groups that are perceived to be close to government and/or stack up on debt. Among the signals that were set to amber, if not red, for some time were the complex group structure, opaque and concentrated ownership partially via offshore fund vehicles, stellar stock price performance driven on limited liquidity or broad institutional and retail ownership, out of line valuations with other similar infrastructure-focused names, high levels of leverage and famously close political relationships over two decades with the most senior leadership of Adani's home State of Gujarat and then the Federal Government in New Delhi. Here was a 'Conglomerate' with multiple listed subsidiaries which seemed to enjoy a Holding company 'premium' rather than the normal discount -it did not add up.

When Adani reversed the fund raising as its previously elevated share prices collapsed, it became main stream news all over the global financial media. Yet it was the confluence of the Hindenburg Report, the reversed share issue, the appeal to nationalism and the proximity to Politics that made it such an interesting story, while leading some editorials to question whether this was a dangerous spoke in the wheels of India's reputation, just as it took on the rotating leadership of the G20.

It has now become a political hot potato in India as the weak and fragmented Opposition parties unite in Parliament to berate the Government on the issue, fuelled by the fact that it took a foreign research report to put it into such sharp relief. It is ironic, therefore, that In India itself the issue had been 'hiding in plain sight' rather than 'visible in hind sight.'

Adani's Achievements and Questions of Risk

Supporters of Adani point out that the Group has achieved a great deal in building and operating World Class Infrastructure. Visitors to its Mundra Ports and Power Stations, for example, on the Western Coast of Gujarat cannot fail to be impressed by the scale and sophistication of these operating assets. In particular, they have a track record for getting things done while the Indian State sponsored entities which previously dominated infrastructure investment have a more patchy record at best. Still, it is extremely important to examine and understand how they were able to achieve this success, on many levels.

Then there is the question of risk. Does the collapse of Adani Share prices and the failed fund raise -at least part of which was due to pay off scheduled debt repayments to Indian and overseas lenders -create a systematic risk for India's financial system and particularly its Banks? At the moment the jury is out though highly knowledgeable analysts point out that many of the assets are throwing off cash which should mitigate that risk, while India's banks have already been requested by the Reserve Bank to report their exposure, indicating the Regulator's grip is swinging into action as well.

Reputation and 'Headline' risk is certainly an issue. Ironically, while being under-owned by independent Institutional Investors, Adani stocks comprised 6% of MSCI India, 1.6% of the NSE Nifty 50 and 4.6% of the S&P BSE 200 indices on 31-Dec-2022, before the proverbial balloons went up. So if you were exposed to India via index tracking -as some large and well known international investors who also have famously high ESG standards -you had exposure to Adani. When the news broke, some of those caught short moved quickly to reduce this exposure exacerbating the share price rout. Now MSCI itself is reviewing the reality of the 'free float' in Adani names and a weighting cut is likely.

Then there is the financial risk, for example that the group cannot service its debt. That has already been mitigated by a payment just made to a number of international Banks. Also, analysts will need to scrutinize the complex accounts with greater forensic detail to verify the validity of reporting, particularly as international press coverage has also drawn attention to the Auditors employed by the group, some of whom are outside the 'Big Four.'

Mitigating Broader India Risk

Moving to the broader 'India risk' that the Adani episode has highlighted. Well, the rest of the World has their share of risk too. The Wirecard CEO is due to depose in a German Court this week; Enron, Worldcom and Bernie Madoff are among the USA's own 'rogue's gallery while in the UK the somewhat vintage Polly Peck Scandal was also a tale of overleverage and opacity. Recent cases of politically connected companies apparently making excess profits from Covid PPE contracts perhaps demonstrate that 'crony capitalism' is also alive and kicking in the Mother of Parliaments. In most of these cases the regulators or auditors were accused of sleeping at the wheel.

What is somewhat different in India the historic backdrop of capital controls and the means devised to avoid them which are echoed in the alleged 'round tripping' of funds back into India , the concept and power of corporate 'promoters', the specter of 'crony capitalism' and close nexuses with politicians that adds another layer of complexity into the process of choosing investable companies and Groups.

You need a mechanism in place to manage all of these risks from the outset. At Quantum we have had our 'Integrity Screen' as a filter since 1996. This has meant that we have avoided many, if not all of these names including Adani. Importantly, that is the first filter after which we then take a closer look at Valuation and Liquidity parameters. Only then will broader ESG parameters be examined as well. When we do use our proprietary ESG scoring 50% of the weight is on Governance. Unless you can pass the Governance tests -which are multiple -you cannot proceed to the next stage. That is why the G comes first for us in ESG. Recent events have only underlined the importance of this.

Disclaimer

The stock(s) discussed in this article has been featured purely for information/illustration purposes. This is not a recommendation to buy or sell the stock(s).

Related Post

India: T I N A to A N T I

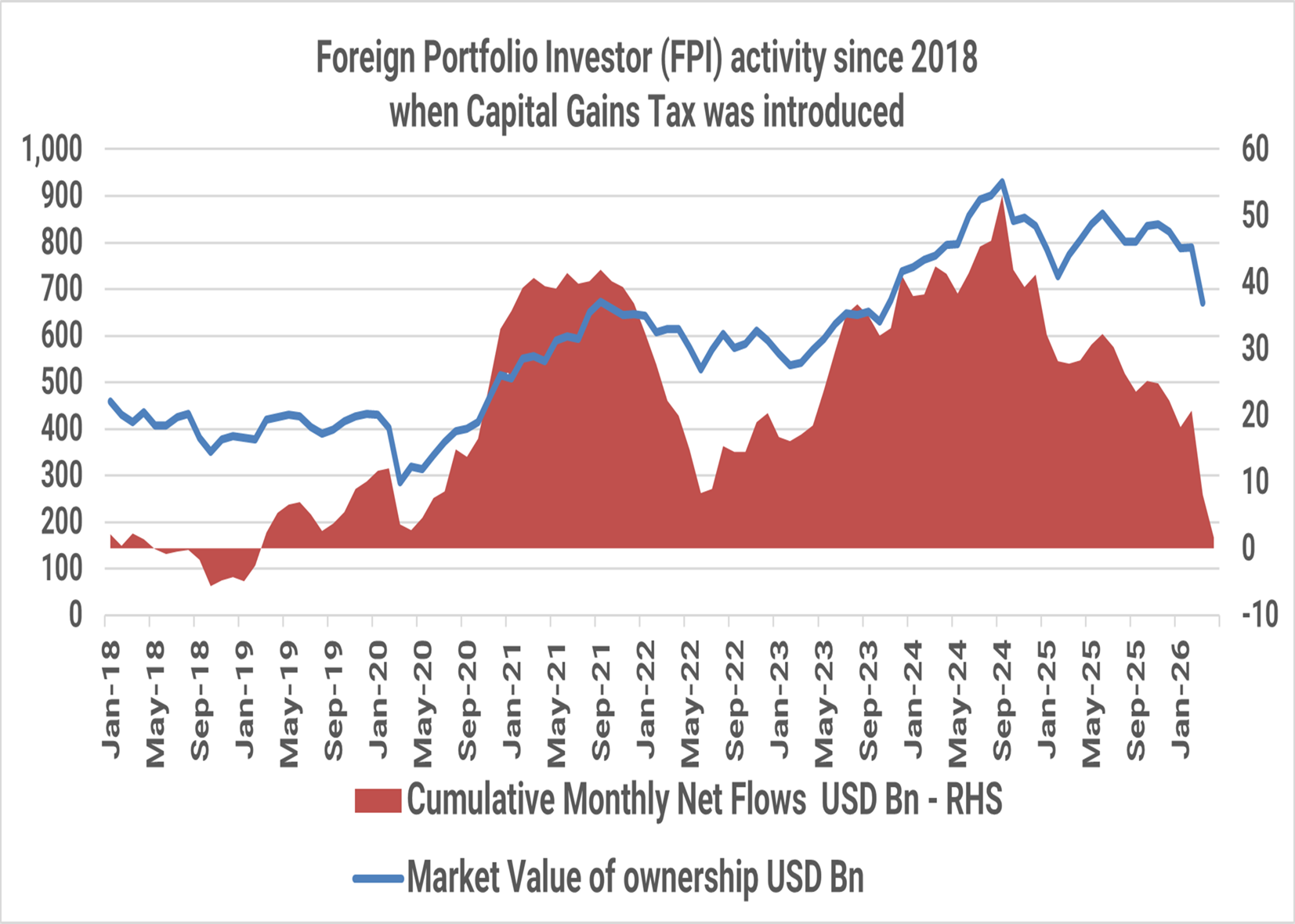

The Indian public equity markets peaked in September 2024. Since then, foreign investors have sold USD 51 billion till April 2026. The market value of foreign investor holding in Indian equities has fallen from USD 930 billion in September 2024 to USD 670 billion, a ~30% drop as at the end of March 2026.

India Investing: From a complicated 2025 to a Simpler 2026?

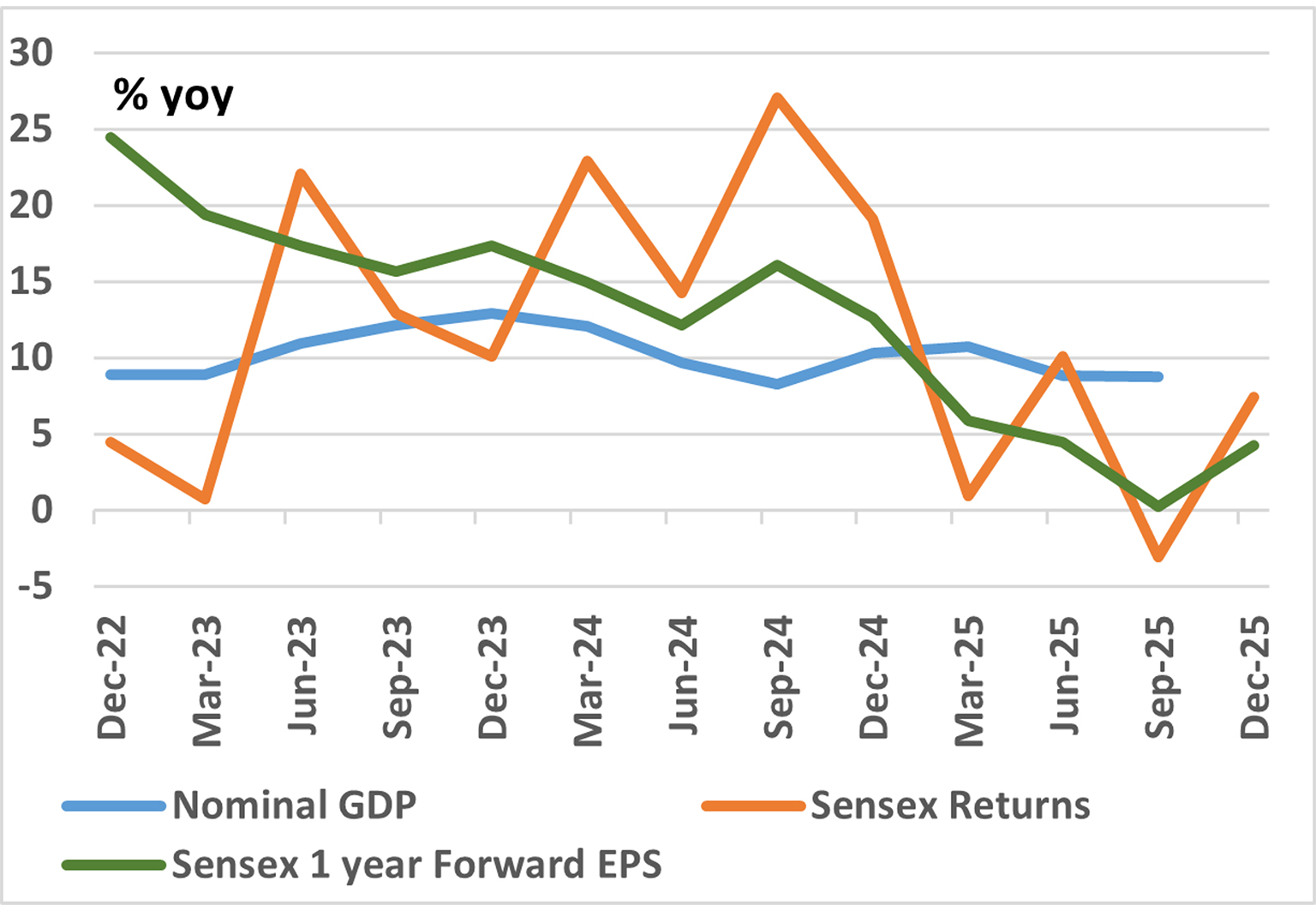

The simple India investing story of double-digit nominal GDP growth reflecting in stock market returns even in dollar terms has faced some headwinds in 2024/2025. Are these headwinds structural? What should investors expect in 2026?

India Investing Under Global Mood Swings

The narrative around global investing is often built around stories. Investors weave these stories around cycles, themes, and opportunities to justify and support their investment rationale.

The Great India Under-Allocation

The most common response to our reach outs to prospective Global Investors to get them interested in Indian Equities is ‘NO’ response.

Our Strategies

Explore how our two main strategies – Predictable India Equity and India Integrity Equity - with demonstrated success of our tried and tested research and investment processes can ensure your India equity allocation will have higher predictable outcomes and no surprises.

Q India Value Equity Strategy

20+ years of India Long-only, Liquid, High-Governance, Margin of safety = Predictability

Integrity screen since 1996, strategy Track record since 2000.

Q India Responsible Returns Strategy

Liquid, proprietary Integrity Scores, Financial Soundness

Integrity Screen since 1996, enhanced criterion since 2015, strategy Track Record since 2019; strategy AuM: $9.7 mn Mandate Capacity: $5 billion

Quantum Advisors pioneered a quantitative as well as qualitative analytical approach to equity investing in India, providing for the first time, consistently applied valuation metrics to evaluate investment opportunities in India’s emerging stock markets. Over the years, Quantum Advisors has continued and enhanced its tradition of extensive financial analysis and value investing, as it has evolved into an investment advisor and asset manager.

Our investment philosophy and strategy involves the use of intensive qualitative and quantitative fundamental analysis. We build and monitor our clients’ portfolios actively while at the same time avoiding excessive trading, and control risk by endeavoring to keep our clients’ portfolio adequately diversified, both in terms of the sectors included in those portfolios, as well as with respect to the level of concentration in any specific security.