Two years ago, did you know what you would have for lunch today?

Well, two years ago we estimated what the value of your portfolio would be today!

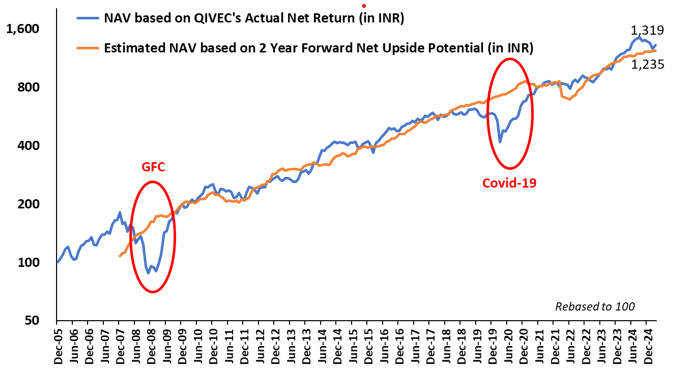

In the dynamic world of finance, where uncertainty often holds sway, Q India Value Equity Strategy carves a niche for itself, presenting certainty born out of a robust research and investment process. While equity investment outcomes can be unpredictable, Quantum's commitment to a disciplined approach emerges as a beacon of stability in the financial landscape. One compelling piece of evidence attesting to Quantum's prowess is the Unique Estimated Upside Potential chart, a visual testament to the alignment of past estimation with present. This chart, diligently estimated every month since December 2005, stands as a testament to Quantum's commitment to transparency and accuracy. Providing estimates of the Portfolio's NAV two years forward, the chart is a unique tool that unveils the potential to deliver in line with the upside in an investment.

The Outcome of our Disciplined Research and Investment Process has a great ‘Fit’: ‘Stirred, Not Shaken’ by two massive Global Macro Events: GFC and Covid

Source: Quantum Advisors, As of March 2025; Please refer to Disclosure 7 for methodology of calculation/other information to understand the criteria, assumption, risks & limitations. We do not guarantee that the Upside Potential indicated above for the future will actually be achieved and the actual returns may or may not be in line with the estimated upside potential, including the possibility of the loss. Past performance does not guarantee and is not indicative of future results. The value axis has been plotted based on logarithmic scale of 2.

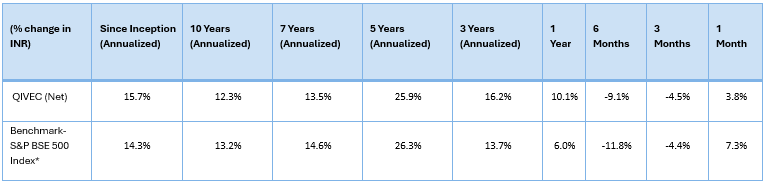

Delving into the chart's revelations, we discover significant consistency. The estimated net increase of 12.4 times in 19 years since December 2005, at a robust 13.9% CAGR, mirrors the actual growth of the composite NAV, which increased by 13.2 times at a 14.3% CAGR over the same period. The S&P BSE 500 TRI benchmark return for the same period was 13.4%. In a world where certainty is rare, Q India Value Equity Strategy has consistently delivered on its estimation and is unshaken by the turbulence of unpredictable markets.

(All the return numbers in the above paragraph are in INR)

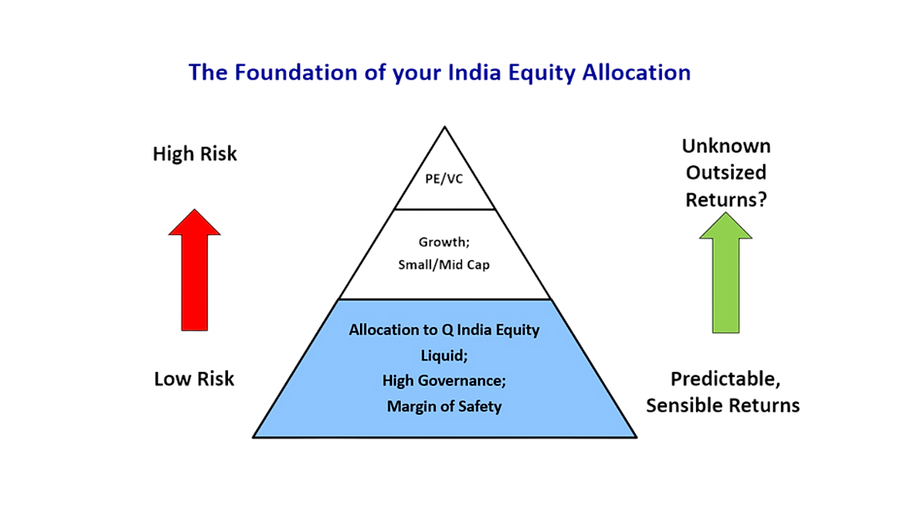

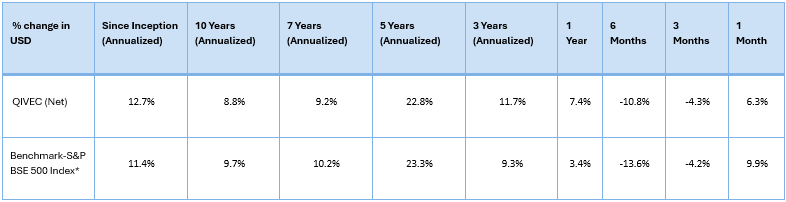

The Quantum India Value Equity Strategy (QIVEC) has a total track record going back to the year 2000. Its goal is to generate sensible and predictable returns in a liquid, scalable, high-governance portfolio, which is built with a margin of safety.

The research process filters for stock liquidity, removes companies which do not meet our management integrity screen and then looks for margin of safety in valuations.

We value stocks on a rolling 2 or 2.5-year forward basis on a normalised median valuation.

We then try to buy at a minimum 25% discount to that forward intrinsic value. So if we are right, the upside potential over a 2 year period = 25/75 = 33.33% over 2 years = 15.5% CAGR on a gross basis.

If we show the above chart in gross terms, the estimated gross returns in INR should have increased by 15.7 times in 19 years (since December 2005) for a 15.4% CAGR till March 2025. The actual gross increase in the portfolio for the same period is 16.7 times for a 15.7% CAGR.

It is indeed remarkable how the process is predictable over such long time periods.

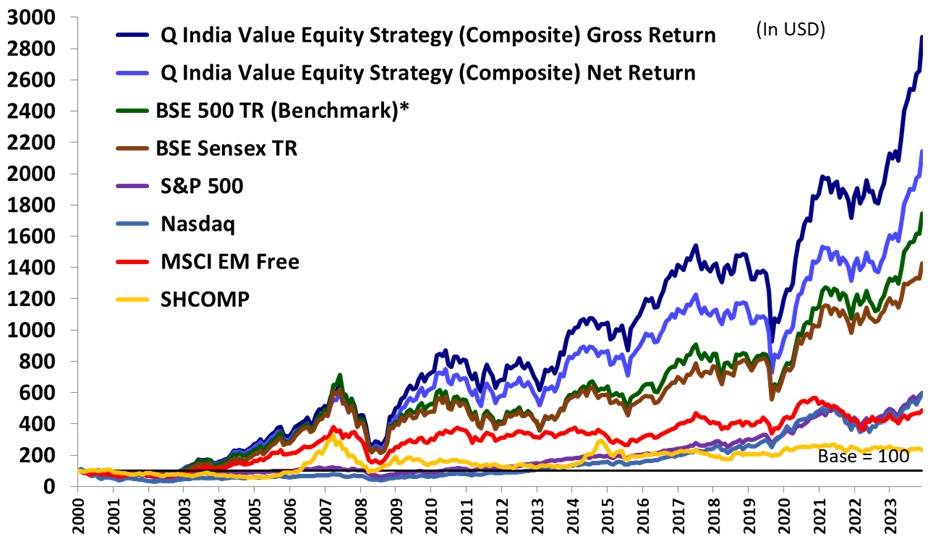

Quantum India Value Equity Strategy through this team-driven, disciplined, bottom-up, proprietary stock selection process has thus generated 13.0% CAGR in US Dollars (as of the end of March 2025), net of fees since August 2000. (The BSE-500 TRI Index (benchmark) returned 11.9% during the same period)

Across 24 Years Of Mood Swings, Quantum India Value Equity Composite Returns 1.8x > S&P 500

In 2005 – India was “BRIC” ; In 2013 India Was “Fragile Five” ; In 2015 India Was “TINA”

Since 2021 India is “China + 1”

Source: Quantum Advisors, Data as at March 2025, rebased to 100 in August 2000

The performance shown above does not guarantee future results and future performance may be lower or higher than the data quoted. Please refer Disclosure Statement for important performance related disclosures and disclaimers. The Quantum India Value Equity Composite (QIVEC)’s inception date is considered as August 01, 2000 as per our internal performance computation policy and procedures. * Effective April 1, 2023, the Benchmark for QIVEC has been changed to S&P BSE 500 TRI as prescribed by SEBI, India. Note- The return shown above are computed as per Quantum’s internal policy and procedure on performance computation. The returns of QIVEC computed in accordance with SEBI guidelines, as applicable from time to time and the computation methodology prescribed in the SEBI guidelines are given in Annexure 1 at the end of this document

So investors who want to roll the dice and are not bothered about governance and valuations can of course buy the Indian indices and other growth managers. However, if they do care about reputation risks and the risks of valuations in India, and desire certainty in an uncertain world, Quantum should be their core allocation.

Disclosure Statement

- Q India Value Equity Composite (Composite) is an aggregation of Client portfolios under the Q India Value Equity Strategy with a similar investment mandate and with no cash restrictions that are managed or advised by Quantum Advisors on a discretionary basis using the long only value equity strategy. The Composite does not include all client portfolios due to various client-imposed portfolio restrictions, even though all portfolios in this broad mandate are managed using the same strategy. The Composite represents 0.05% of the total AUM under the Q India Value Equity Strategy as on March 31, 2025.

- Composite Gross return stated above are the returns achieved before the deduction of all fees and expenses except trading cost. Composite’s Net returns are computed net of fees and expenses. All returns stated above are assuming reinvestment of all dividend and other earnings. Returns from cash and cash equivalents held in portfolios are included in the return calculations.

- The various constituents of the Composite pay different management fees. The net-of-fee and expense returns of the Q India Value Equity Composite indicated in tables in this newsletter reflect the weighted average management fees paid to Quantum Advisors Pvt Ltd (QAPL) by the different constituents of the Composite.

- As the different constituents of the Composite are subject to different management fee structures, the actual performance experienced by a constituent of the Composite may be worse or better than the net-of-fee-and-expense returns of the Composite.

- The return shown in the graphs in this document are calculated using Time Weighted Rate of Return (“TWRR”) method.

- The firm has formulated an internal policy and procedures on inclusion, exclusion of the portfolio accounts and factoring significant cash flows for computing the performance of Composite which will be available upon request.

- Upside Potential of Q India Value Equity Composite - methodology of calculation and other information to understand the criteria, assumptions, risks & limitations - The referenced Upside Potential shows the two years forward estimate of rebased NAV on the basis of upside potential of the Q India Value Equity Composite portfolio (“Value Composite”). Upside Potential is equal to the sum total of [weight of each stock in the portfolio (multiplied by) the percentage difference between the current market price and the Sell limits assigned to the stock by our in-house Research team].

We use various metrics to value companies based on different valuation ratios such as Dividend yields, price to earnings, price to cash flow, price to book value etc. While valuing the companies, we take in to account the environment in which they operate, their management quality, their financial strength and other fundamental criteria, their historical valuation and peer group valuation. Sell limit of a stock is our research team’s long-term assumptions on the intrinsic value of the company, estimated typically on a 2-year forward basis. The valuation of a company is done on the basis of normalised assumptions. It means that we do not value the companies on the basis of peak or trough margins.

However, we do not guarantee that the Upside Potential indicated above for the future will actually be achieved and the actual returns of an individual client account may or may not be in line with the estimated Upside Potential of the Composite portfolio, including the fact that there exists a possibility of loss.

The computation of Upside Potential is dynamic in nature and varies based on factors such as change in market prices of the stocks, change in portfolio composition due to investment decisions by the portfolio manager or due to corporate actions at issuers, and revisions in Sell limits assigned to the stocks by the Research Team due to changes in various macro-economic as well as company/industry specific factors. The computation of rebased NAV 2 years forward is based on assumption that the current portfolio composition and the fees and expenses of the account remain unchanged, and the current Sell Limit of the stocks converges into actual market price at the end of the period.

Past performance does not guarantee and is not indicative of future results. Future performance may be lower or higher than the data quoted, including the possibility of the loss. - The returns of individual client accounts may vary from the returns of the Composite on account of difference in fees and expenses charged to each of the client accounts and any cash or stock level constraints imposed by the client on the portfolio manager’s discretion.

- The "Index" is a product of Asia Index Private Limited (AIPL), which is a joint venture of S&P Dow Jones Indices LLC or its affiliates (“SPDJI”) and BSE has been licensed for use by QAPL. Standard & Poor’s® and S&P® are registered trademarks of Standard & Poor’s Financial Services LLC (“S&P”); BSE® is a registered trademark of BSE Limited (“BSE”); and Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”). © Asia Index Private Limited 2021. All rights reserved. Redistribution, reproduction and/or photocopying in whole or in part are prohibited without written permission of AIPL. For more information on any of AIPL’s indices please visit http://www.asiaindex.com/. None of AIPL, BSE, Dow Jones Trademark Holdings LLC, their affiliates nor their third party licensors make any representation or warranty, express or implied, as to the ability of any index to accurately represent the asset class or market sector that it purports to represent and none of AIPL, BSE, S&P Dow Jones Indices LLC, Dow Jones Trademark Holdings LLC or their affiliates nor their third party licensors shall have any liability for any errors, omissions, or interruptions of any index or the data included therein.

- S&P BSE 500 is a free-float-adjusted, market-cap-weighted index of 500 companies listed on the Bombay Stock Exchange.

- S&P BSE 500 comprises of stocks which are highly liquid (predominantly Large Cap) and broadly covers our investment universe under this investment strategy. Hence, we believe it makes a good benchmark as the portfolio has a bias towards highly liquid stocks. However, the Composite’s performance may not be strictly comparable with the performance of the Benchmark, due to inherent differences in the construction of the portfolios, and the volatility of the benchmark over any period may be materially different than that of the composite over the same period.

- The firm sources benchmark-related data from Bloomberg.

- Data of other indices is provided for information purposes only and to allow investors to compare the performance of the Composite to that of certain indices (many of which are well known and widely recognized). While we generally believe these comparisons provide meaningful and useful information to investors (for example, as a way of comparing an investment in the Composite to other types of investments that investors might make), inclusion of any particular index is not a representation that the index is an appropriate benchmark for evaluating the Composite’s performance. In particular, the volatility of indices over any period may be materially different from that of the Composite over that same period.

- All INR to USD conversion has been done based on RBI FX Rates till May 2010, and WM Reuters Closing Spot Rates (4pm UK time) from June 2010 onwards.

- This monthly report is strictly for information purposes. Investments in the Portfolio Account are not guaranteed or insured and are subject to investment risks, including the possible loss of the principal amount invested. The value of the Portfolio Account and the income from it may fall as well as rise. Past performance is not necessarily indicative of future performance. QAPL reserves the right to make any changes and corrections to its opinions expressed in this document at any time, without notice. Information sourced from third parties cannot be guaranteed and has not been independently verified. Comments made herein are not necessarily indicative of future or likely performance of the Portfolio Account and are based on information and developments as on March 31, 2025, unless otherwise stated.

- All of the forward-looking statements made in this communication are inherently uncertain and QAPL cannot assure the reader that the results or developments anticipated by QAPL will be realized or even if realized, will have the expected consequences to or effects on, us or our business prospects, financial condition or results of operations. A prospective investor can generally identify forward-looking statements as statements containing the words “will”, “should”, “can”, “may”, “believe”, “expect”, “anticipate”, “intend”, “contemplate”, “estimate”, “assume”, “target”, “targeted” or other similar expressions. Readers are cautioned not to place undue reliance on these forward-looking statements in making any investment decision. Forward-looking statements made in this communication apply only as of the date of this communication. While we may elect to update forward-looking statements from time to time, we specifically disclaim any obligation to do so, even if internal estimates change, unless otherwise required by applicable Securities laws.

Annexure 1

Table: Performance of the Q India Value Equity Composite (QIVEC) computed as per methodology prescribed under SEBI guidelines

Inception Date: June 27, 2000; Source: Quantum Advisors and Bloomberg Finance LP; Data as of March 31, 2025.

* Effective April 1, 2023, the benchmark for Composite has been changed to S&P BSE 500 TRI.

Disclosure Statements:

1.Composite inception date is taken as the date on which the Portfolio Account is funded by the Client and accrual of Management fees commences.

2.All INR to USD conversion has been done based on RBI FX Rates till May 2010, and WM Reuters Closing Spot Rates (4pm UK time) from June 2010 onwards.

3.The performance shown above does not guarantee future results and future performance may be lower or higher than the data quoted.

4.Recipients may check the relative performance of investment approach offered by other Portfolio Managers under the same strategy by clicking here.

Brief note on performance computation methodology under SEBI guidelines:

SEBI has prescribed specific guidelines on computation and disclosure of performance by portfolio managers to their clients and in marketing materials. A summary of these guidelines is given below:

- The performance of a discretionary portfolio management mandate shall be calculated using Time Weighted Rate of Return (“TWRR”) method.

- Cash holdings and investments in cash equivalent are considered for calculation of performance.

- Performance computed and reported shall be net of all fees and all expenses (including taxes/statutory levies thereon).

Statutory Disclosures:

- The performance reported above is not verified by SEBI

- Quantum Advisors provides a direct on-boarding option to clients who wish to avail our services, without intermediation of persons engaged in distribution services.

- For detailed description of Q India Value Equity Strategy such as investment objective, assets allocation pattern, investment strategy and philosophy, associated risk factors and other details please refer to the Disclosure Document available at www.qasl.com.

Important Notice:

This newsletter contains hyperlinks to websites operated by third parties. These linked websites are not under the control of QAPL and are provided for your convenience only. Clicking on those links or enabling those connections may allow third parties to collect or share data about you. When you click on these links, we encourage you to read the privacy notice of the website you visit. QAPL does not endorse or guarantee products, services or advice offered by these websites.

UK related important disclosures

The content of this article has not been approved by an authorised person within the meaning of the Financial Services and Markets Act 2000 (“FSMA 2000”). Reliance on this article for the purpose of engaging in any investment activity may expose you to a significant risk of losing all of the property or other assets you invest or of incurring additional liability. This article is exempt from section 21 FSMA 2000 on the grounds that it is directed only to certified sophisticated investors, high net worth companies, unincorporated associations, trusts and/or investment professionals within the meaning of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (“FPO”). The investment activity described in this article is only available to these persons or entities and no other person or entity should rely on the contents of this document.

The protections conferred by or under the Financial Services and Markets Act (FSMA) will not apply to this article and any investment activity that may be engaged in as a result of this article. The applicability of any dispute resolution scheme or compensation scheme and its jurisdiction (if and where applicable) pertaining to a transaction resulting from this article would be as specified in the respective client agreements.